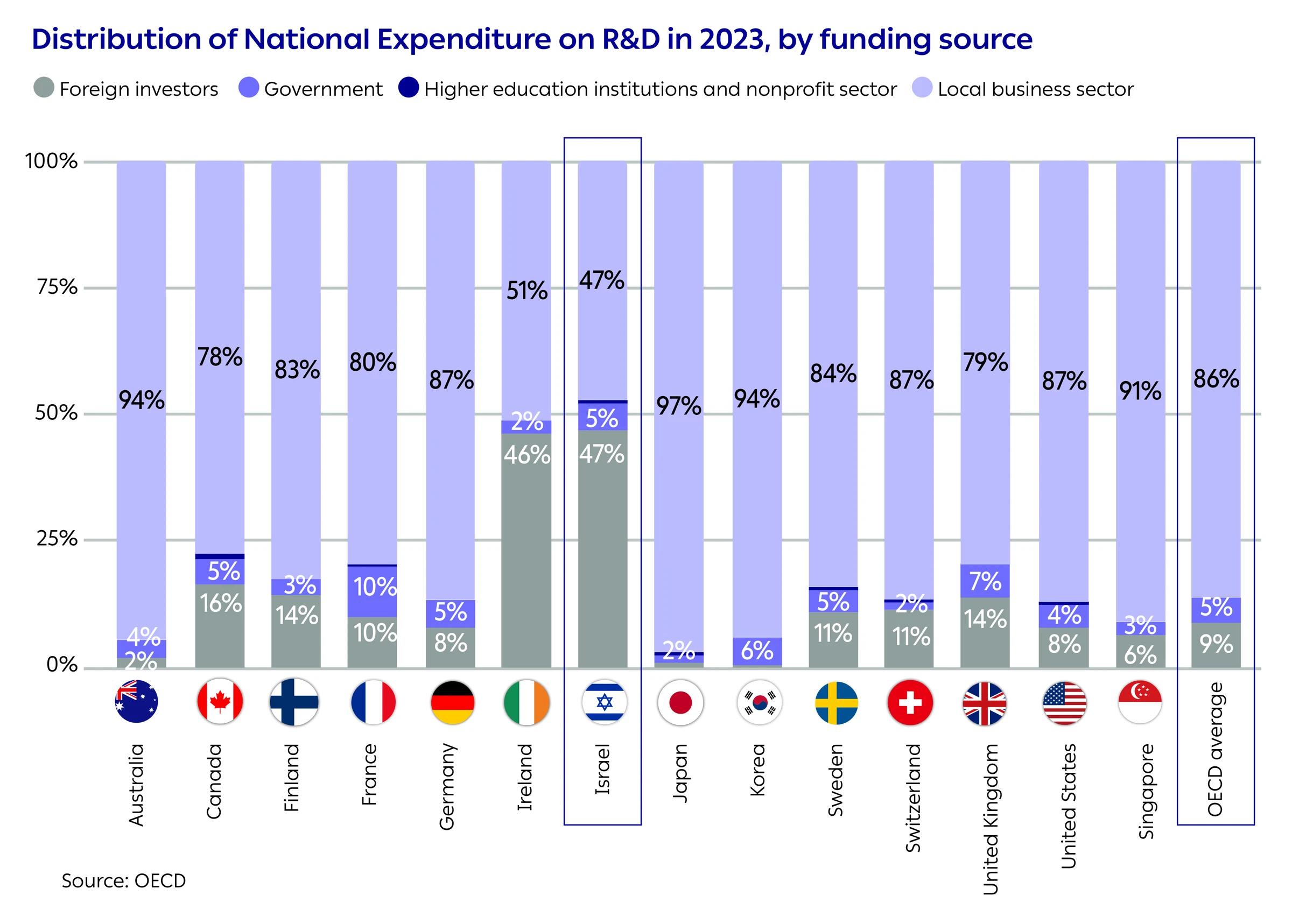

47% of R&D in Israel in 2023 Was Funded by Foreign Investors

The chart here presents the distribution of expenditure on research and development (R&D) in the business sector by funding source.

Total expenditure in each country represents 100% of investment in business-sector R&D, divided into four main sources: the local business sector, foreign funding, state funding, and higher education institutions and the nonprofit sector.

Foreign funding includes investments originating outside Israel, such as international venture capital funds, foreign corporations, foreign institutional investors, and overseas public entities. It is important to note that investments by Israeli venture capital funds are, to a relatively large extent, funded by foreign investors.

The data shows that in Israel, the share of foreign funding in business-sector R&D is particularly high, standing at 47% of all business-sector R&D funding, compared with the OECD average of 9%. This figure indicates a high dependence on foreign investment as a key source of funding for Israeli companies’ innovation activity.

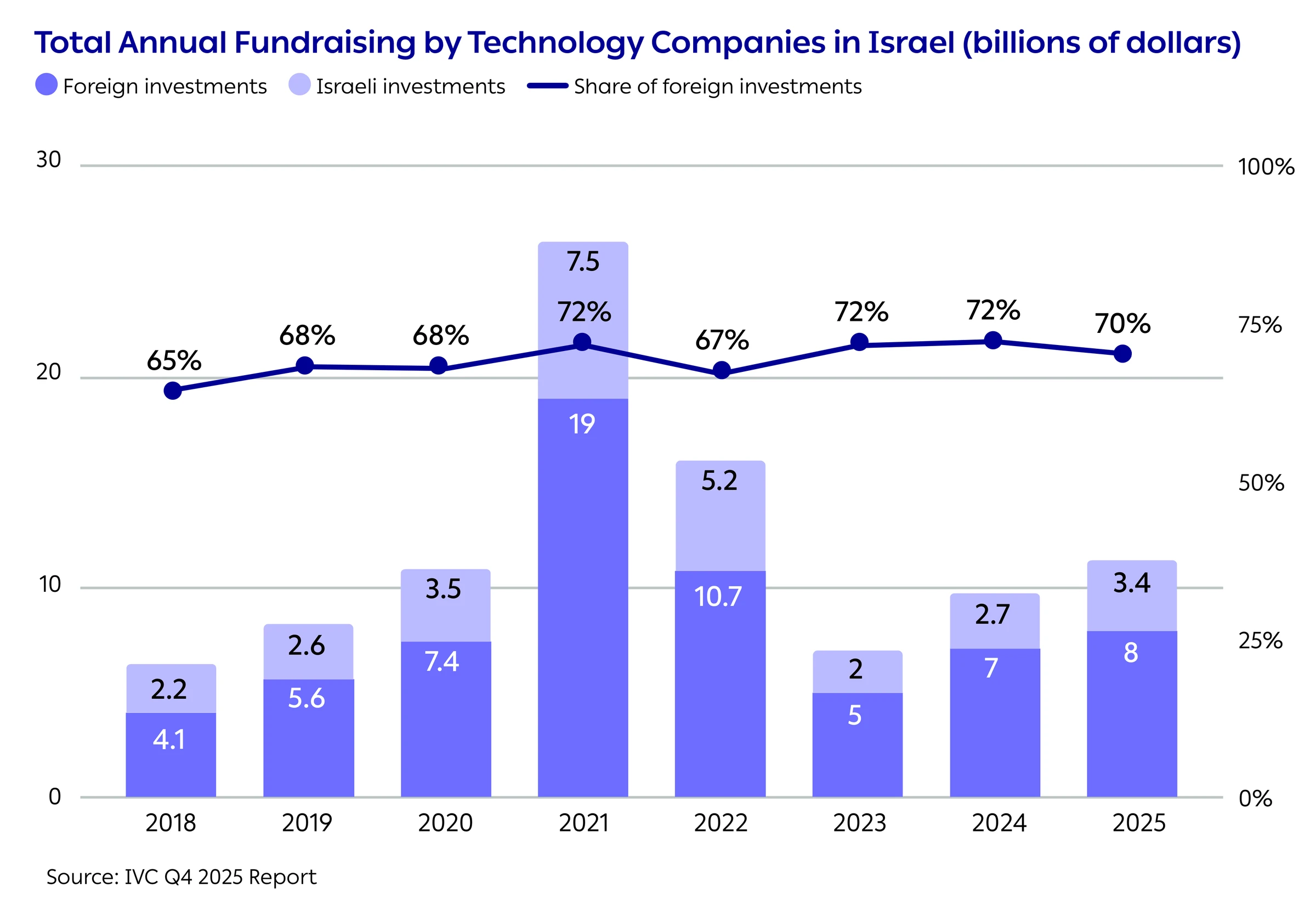

70% of Venture Capital Investments in Israel in 2025 Were Conducted by as Foreign Investors

When focusing solely on venture capital investments in high-tech companies, the share of foreign investments rises to 70% of total invested capital and has remained at an almost identical rate over the past seven years. In this analysis, investments were classified as foreign when the investing entity’s headquarters address was outside Israel. This does not, for example, refer to investments by foreign LPs in Israeli VC funds.

The dominance of foreign investors reflects, on the one hand, the relative advantage and attractiveness of Israeli high-tech, and, on the other hand, a certain risk stemming from its heavy dependence on foreign funding.

However, the data shows that during periods of instability, specifically in 2023-2024, the share of foreign investors increased. Moreover, the decline in the scope of investments by Israelis in Israeli high-tech was also sharper than the decline in foreign investments: foreign investments decreased by 53% in 2023 compared with 2022, while Israeli investments decreased by 62% during the same period.

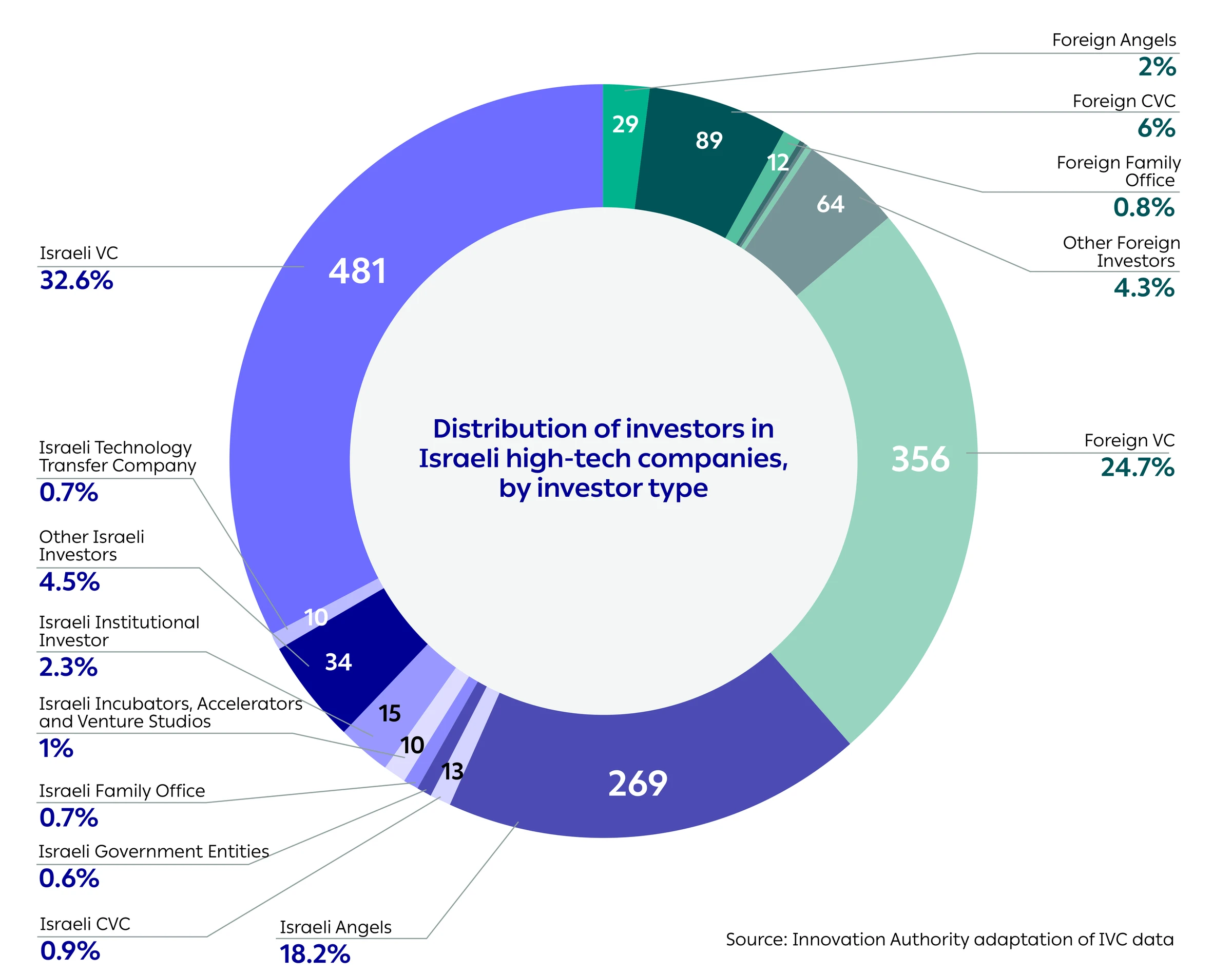

61% of Active Investors in Israel in 2025 Were Israeli, Most of Them Venture Capital Funds

Although most of the capital invested in high-tech in Israel comes from foreign investors, most investors in Israeli high-tech are Israeli.

In total, 481 Israeli venture capital funds were active in 2025, alongside 269 Israeli angels.

Foreign venture capital funds are the second-most dominant investor group in Israel, accounting for about 25% of active investors in 2025. The share of foreign angels, by contrast, is much lower than the share of Israeli angels, standing at only 2%.

In addition, 6% of active investors are corporate venture capital (CVC) funds of foreign companies, totaling 89 CVCs. Alongside them are 13 Israeli CVC funds, which account for 0.9% of all investors.

The chart shows the number of each type of investor involved in at least one investment during 2025. It should be emphasized that the number of investors of each type does not reflect the share of total investments or the number of rounds in which they were involved, but only their share of investors that were involved at least once in high-tech investments in Israel.

The number of venture capital funds refers to funds i.e., a specific fund of a venture capital firm, and not the number of active VC firms. On average, among Israeli VC firms, the ratio is about two funds per VC firm.

Definitions

- Incubators, Accelerators, and Venture Studios – including: General Accelerators, Incubators, Venture Studio

- VC – including: Venture Capital Fund, Venture Lending Fund, Venture Capital Management Company

- Institutional Investor – including: Institutional Investor, Bank, Investment Arm or Nostro

- Government – including: Bi-National Fund, Government Agency, Government Fund, R&D Support Program, Bi-Lateral R&D Program

- CVC – including: Corporate VC only

- Angel – including: Angel Club or Group, Angel Syndicate, Angel, Private Investor

- Family Office – including: Family Office only

- Other Investors – including: Private Equity Fund, Secondary Fund, Hedge Fund, Fund of Funds, Debt Fund, Endowment Fund, Academy Fund, Buyout Fund, Investment Company, Holding Company, Private Equity Management Company, Endowment and Foundation, Investment Management Company, Offset Company, Financial Services Company

- Technology Transfer Company – including: Technology Transfer Company

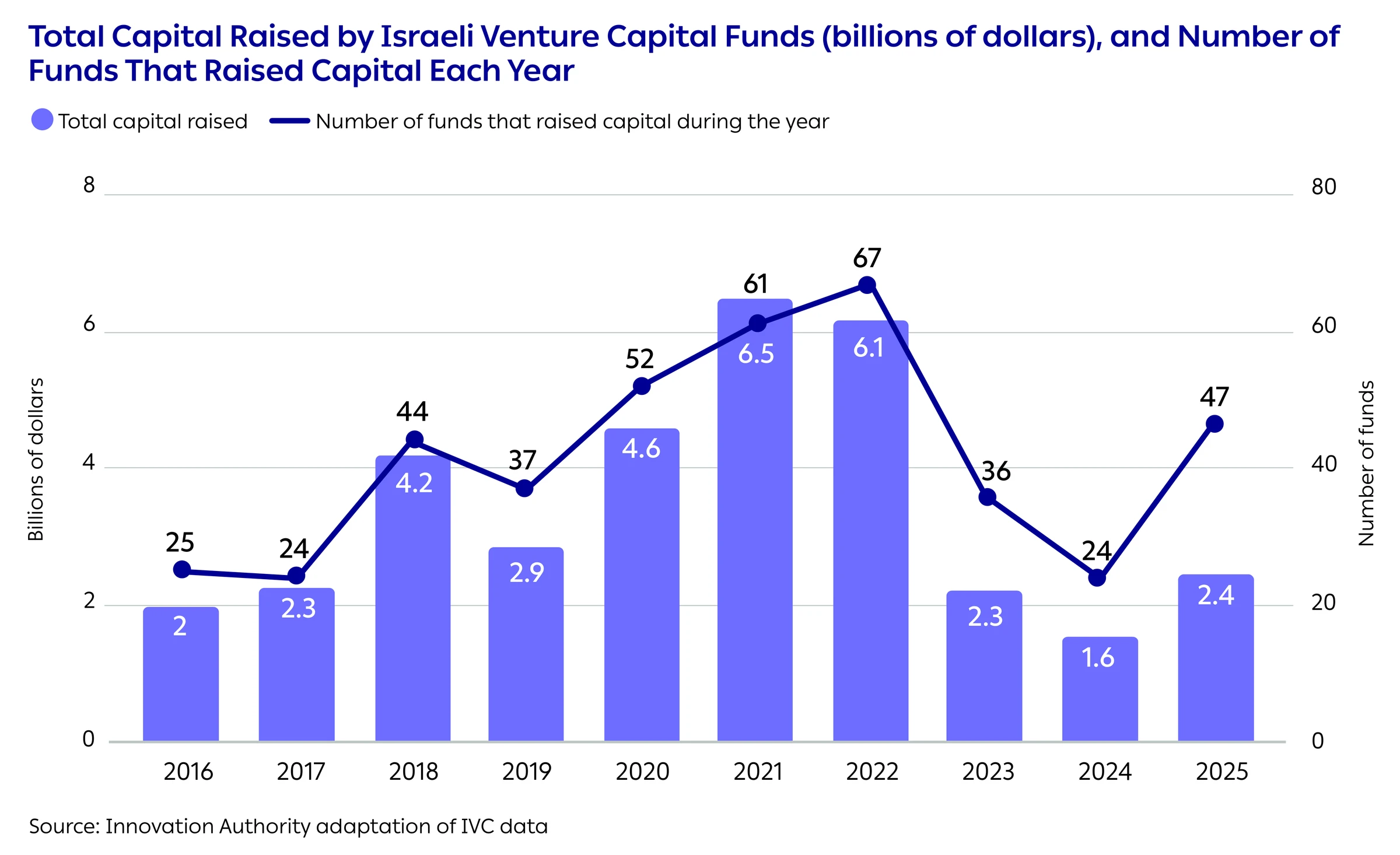

Increase in Fundraising by Israeli Venture Capital Funds in 2025, Alongside a Further Decline in Average Fund Size

After two years of decline in fundraising by Israeli venture capital funds during 2023-2024, the total capital raised by Israeli funds increased in 2025 to a total of USD 2.4 billion. Nevertheless, this amount remains lower than the total fundraising by Israeli venture capital funds in the years preceding the peak fundraising period.

Alongside the increase in total capital raised (a 57% increase in 2025 compared with 2024), the number of Israeli venture capital funds that raised capital almost doubled in 2025 compared to the previous year.

These trends affect the average fund size. While the average fund size in 2016-2022 was about USD 90 million, this figure declined by a third in 2023-2025 to about USD 60 million.

The decline in fund size impacts the scope of capital that can be invested, the opportunities funds have for follow-on investments, and their willingness to take risks.

Since venture capital funds remain the most dominant player in the Israeli ecosystem, a decline in total capital and in fund size among Israeli venture capital funds affects capital availability across the entire industry.

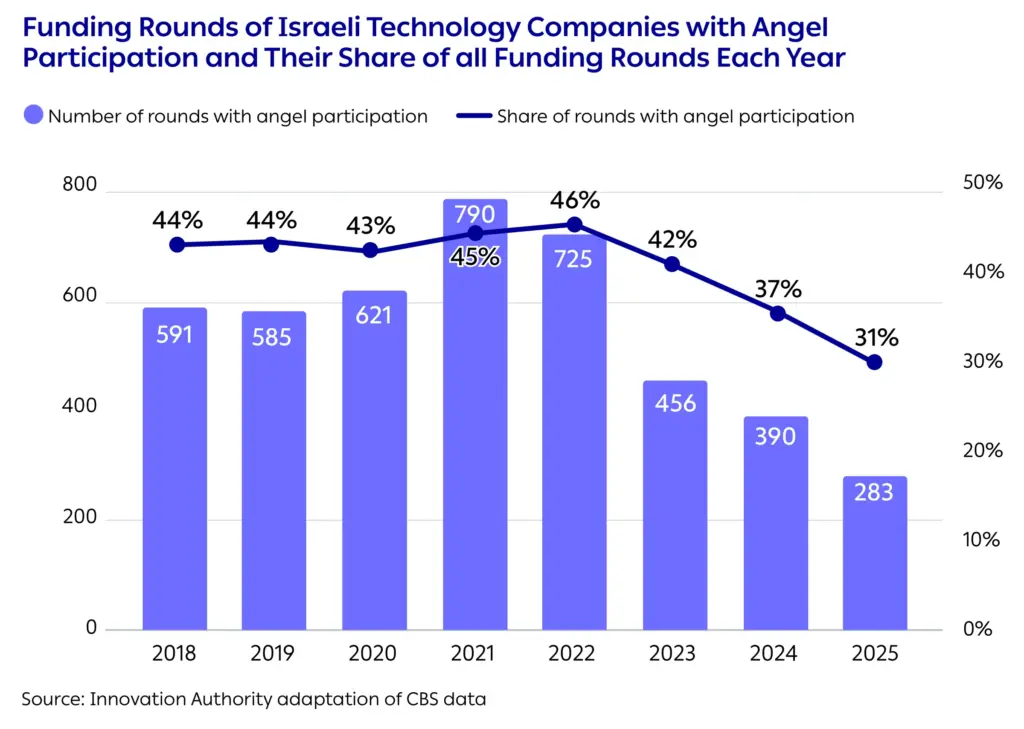

Decline in Israeli Angels’ Participation in Funding Rounds of Israeli Technology Companies Since 2022

In 2025, about 270 Israeli angels (private investors) participated in 280 investment rounds in Israeli high-tech companies.1Analysis of the involvement of angels and other investors in company fundraising focuses on the number of rounds in which they participated and their share. The analysis does not address investment amounts due to the lack of available information on each investor’s share in the round. In many of the rounds, more than one angel investor participated in a single round, and some angels were involved in multiple funding rounds throughout the year.

Between 2018-2023, the share of funding rounds that included Israeli angels remained relatively stable at 40%-50%, however, a subsequent decline was evident in 2023-2025 to a level of 30%-40% of all funding rounds.

The surge in angel investor involvement in 2021 is correlated with the high-tech boom, against the backdrop of the low-interest-rate environment of that period. In the fourth quarter of 2023, there was a decline in both the share and number of rounds that included angel investors, indicating sensitivity to the geopolitical situation and periods of uncertainty. It is very possible, however, that the data for the final months of 2025 will be revised upward due to the late publication of information about fundraising rounds, particularly in small and early-stage investments.

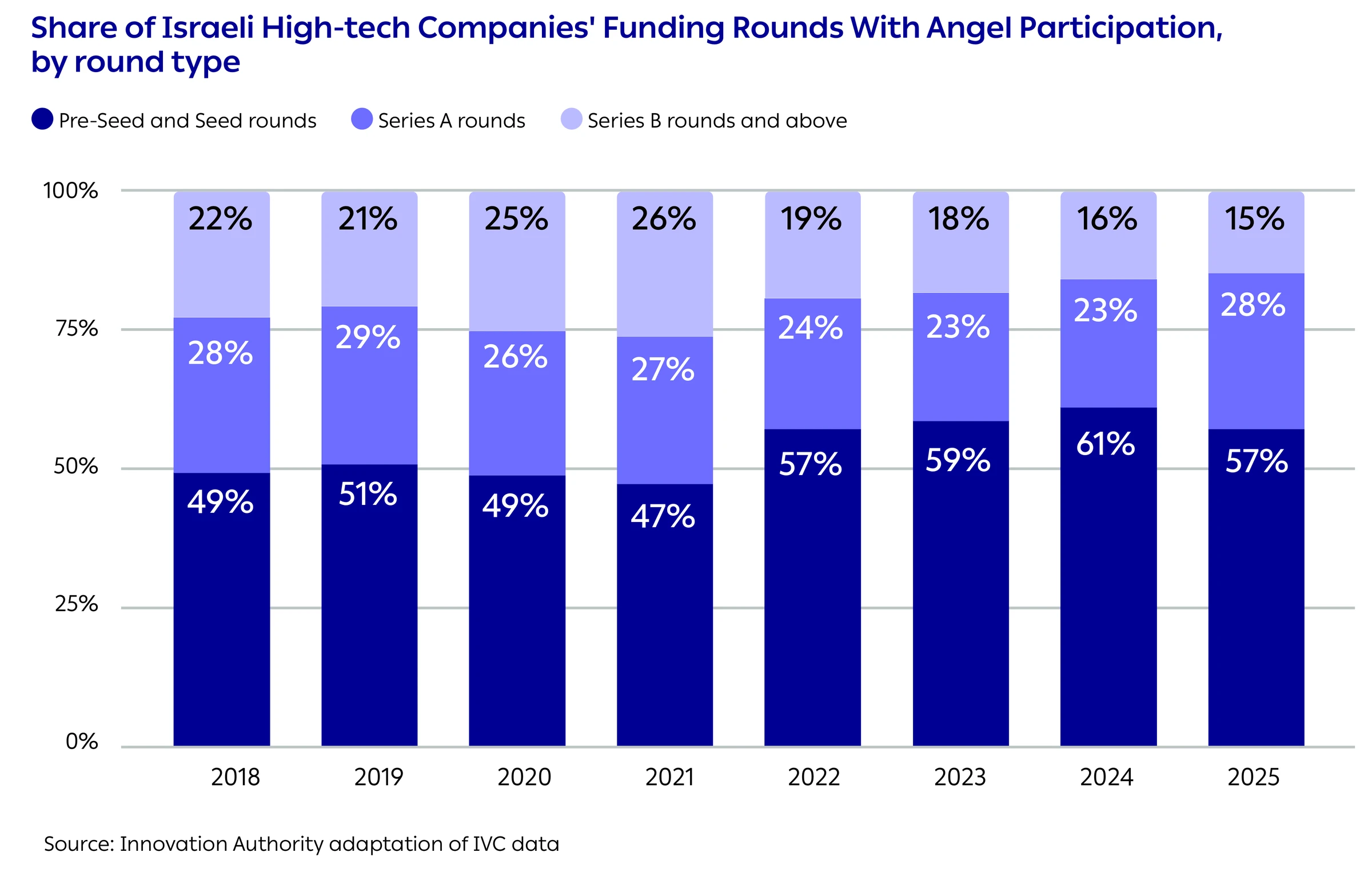

85% of Angel-Backed Funding Rounds are Early-Stage Rounds

Angels usually invest the initial capital in startups and participate in early-stage funding rounds. In 2025, about 85% of investment rounds in which angels participated were in early-stage companies, Pre-Seed, Seed or Series A rounds, totaling 217 investment rounds. At the same time, 15% of angel-backed investment rounds in 2025 focused on later-stage companies, amounting to 37 investment rounds.

Angels’ increased tendency to invest in early stages began in 2022, a year in which the share of early-stage rounds increased from an average of 76% of angel investments in 2018-2021 to an average of 83% in 2022-2025.

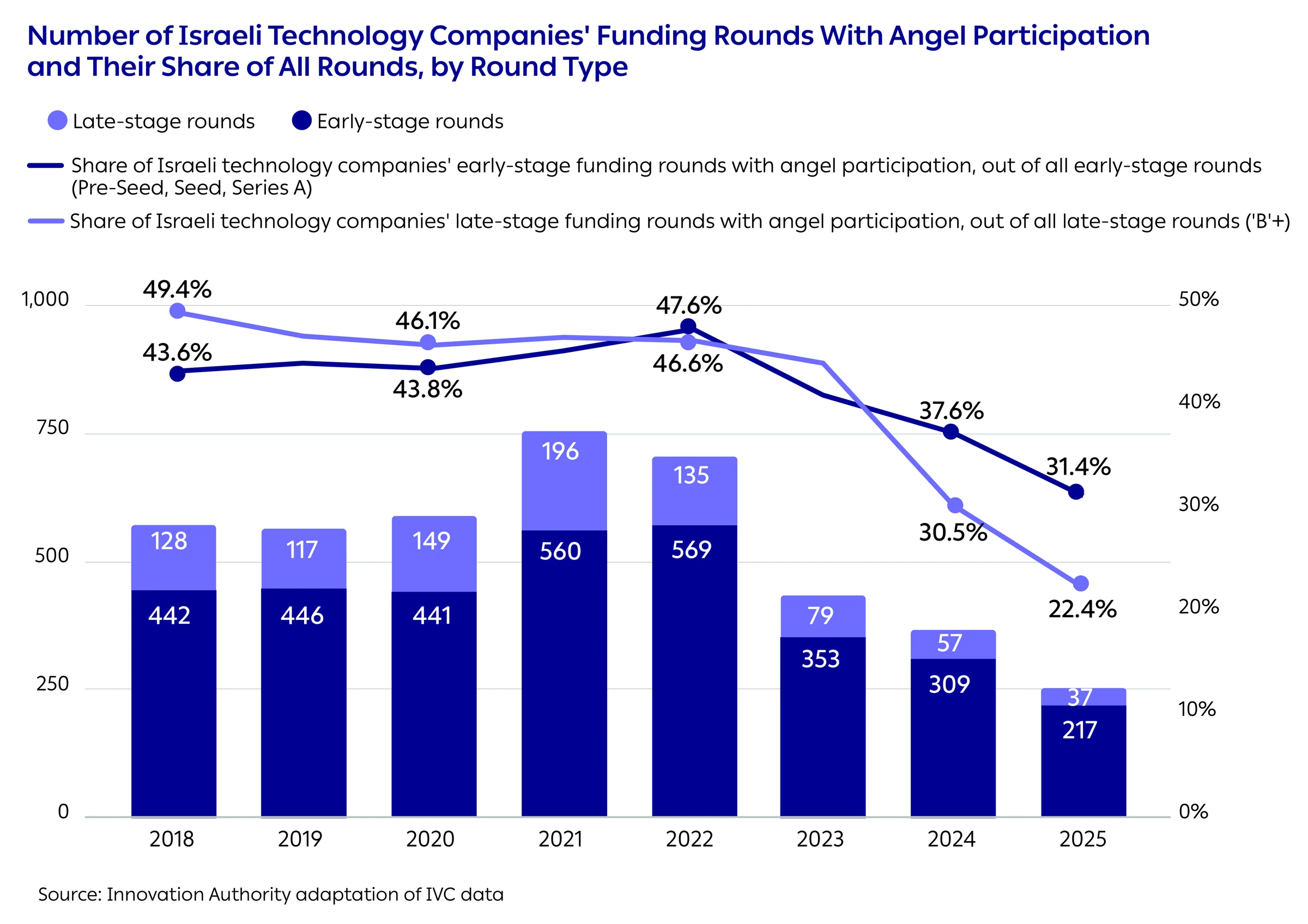

The decline in angel participation in investment rounds adds to the challenging funding environment faced by early-stage startups.

The decline in angel participation in funding rounds intensified in 2023-2025, particularly in later-stage rounds. In 2025, angels participated in only 22% of later-stage rounds (Series ‘B’ and above), down from more than 40% through 2023. This change can be attributed to the increase in the average round size and to the high-interest-rate environment, which made it harder for individual investors who tend to invest lower amounts on average, to participate in these rounds.

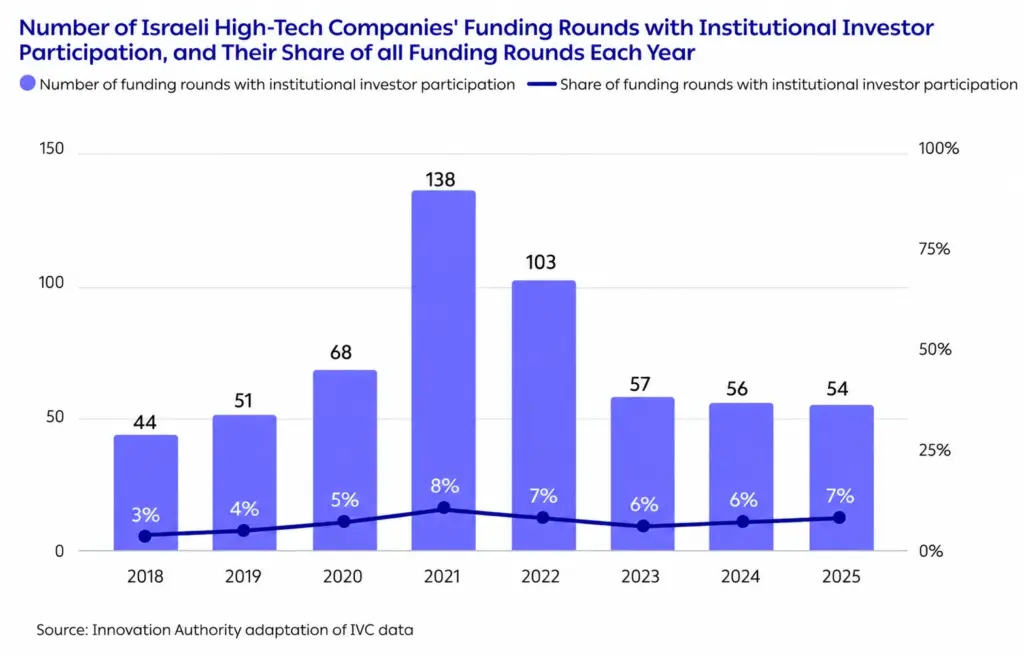

Israeli Institutional Investors Participate Directly in 7% of Israeli High-Tech Companies’ Funding Rounds

Institutional investors invested directly in Israeli startups across 54 funding rounds in 2025, accounting for 7% of all funding rounds that year.2Including rounds in which the amount raised is unknown.

The impact of the decline in interest rates and the high-tech market boom in 2020-2022 is also evident in the volume of institutional investments in high-tech companies. The share of funding rounds with institutional investor participation rose from 3% in 2018 to 10% in 2021, then declined to 6% in 2023, rising again to 7% in 2025.

The total exposure of institutional investors to high-tech is higher than that reflected in the data here because, in addition to direct investments in companies, institutional investors’ capital is also invested indirectly through venture capital funds.

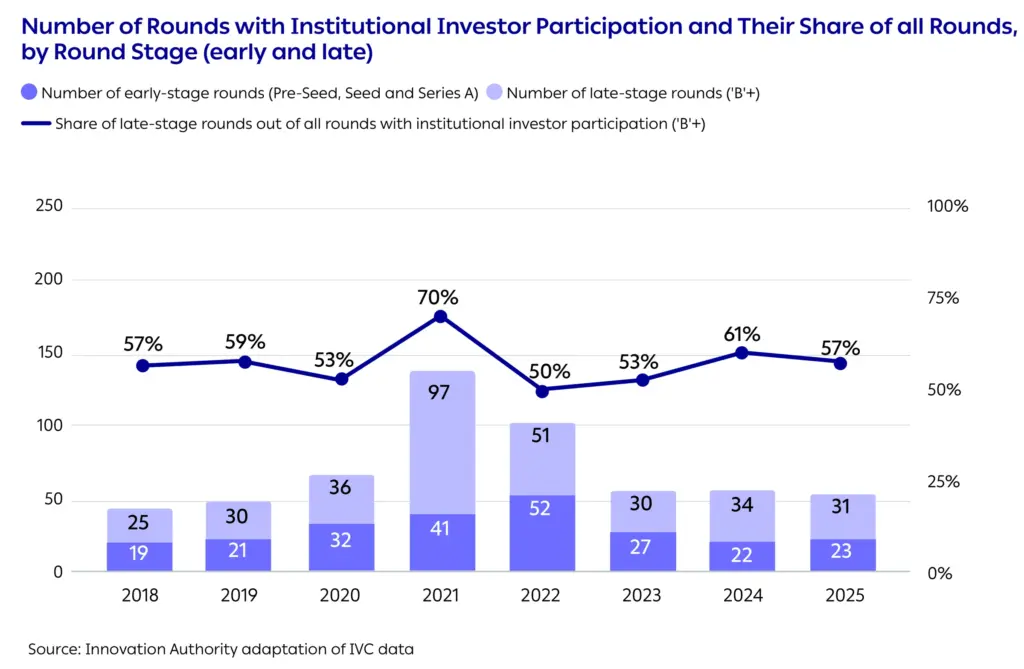

60% of Funding Rounds Involving Institutional Investors Were in Late-Stage High-Tech Companies

Institutional investors tend to seek relatively large investments due to the size of the investment portfolios under their management. Consequently, their investments are primarily focused on later-stage funding rounds (57% of investments in 2025) and on growth-stage companies.

The average round size in which institutional investors participated in 2025 was USD 51 million, compared to an overall average of about USD 28 million per round.