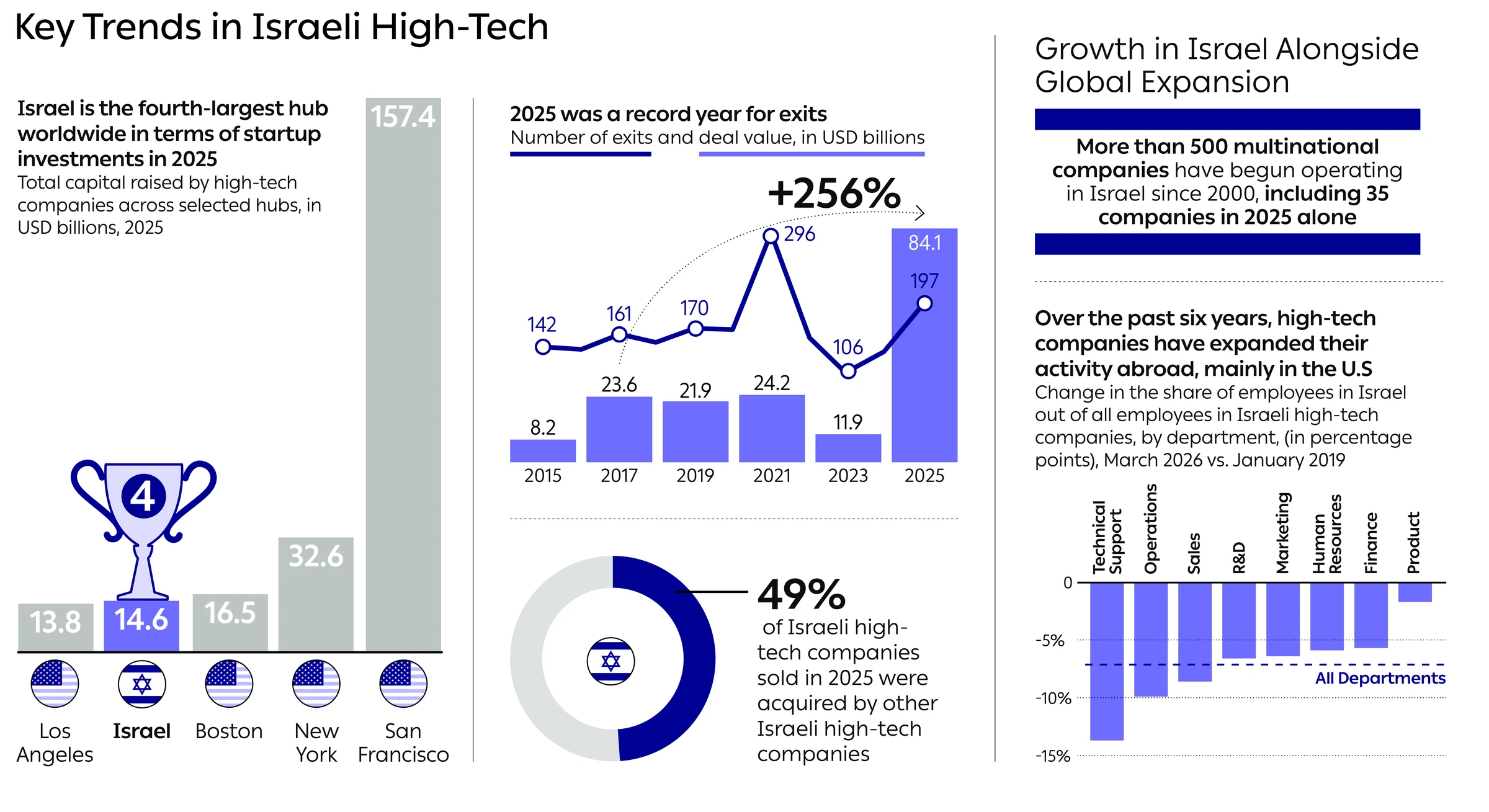

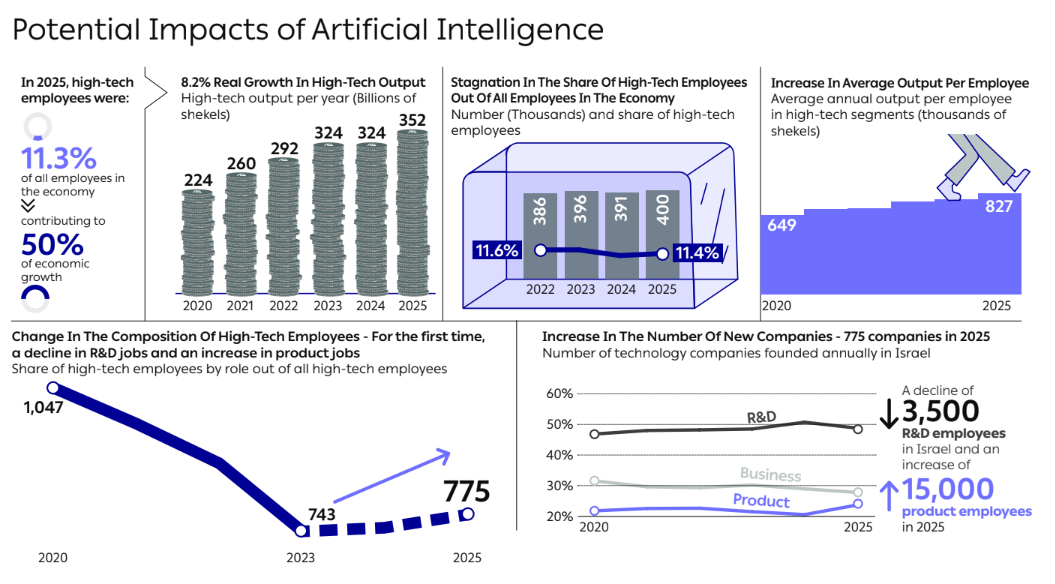

After two years of slowdown in Israeli high-tech, the data presented in this report reflects recovery and return to a growth trajectory in the sector. Despite a complex security and economic environment, the sector demonstrated exceptional resilience and once again proved its strength as the primary “growth engine” of the Israeli economy. High-tech output recorded an impressive growth rate of approximately 8.2%, reached a record share of 58% of total exports, and contributed to around 50% of the overall growth of the economy.

These indicators were accompanied by an increase of 30% in fundraising by Israeli high-tech companies in 2025, compared with 2024; a growth in the number of new high-tech companies to 775; and a record year for exits, with a total value of USD 84 billion in mergers, acquisitions, and IPOs. At the same time, the local high-tech ecosystem continued to establish itself and grow, with additional multinational companies entering the Israeli market and a continued increase in the number of foreign companies acquired by growing Israeli high-tech companies, reaching 81 acquisitions in 2025.

The picture emerging from the current report is not only one of quantitative recovery, but also of a shift in the growth engines of Israeli high-tech. While in the peak years of high-tech (2021-2022), the software development and high-tech services segment led the sector’s growth, 2025 was characterized by renewed growth in the hardware segment (“high-tech industry”). After two years of slowdown in the growth of total high-tech output in 2023-2024, growth in the past year was led by hardware companies, whose output grew by NIS 16 billion (20.7%), a dramatic surge compared with previous years. This trend is also reflected in the composition of high-tech employment, with 8.9% growth in the number of employees in the hardware segments, while software services employment stabilized. It is still too early to assess whether this is a broad structural shift that will continue to affect high-tech output in the coming years.

The impact of artificial intelligence on the future trajectory of Israeli high-tech remains an open question. We are identifying early signs of AI’s impact on labor productivity and on the structure of software companies: a significant increase in output per employee, reaching an average of NIS 793,000 per year, alongside stagnation in employee growth, particularly in the number of developers. In addition, AI has the potential to erode the competitive “moat” of existing software companies while lowering barriers to entry for new companies. This phenomenon may partly explain the increase in the number of new startups established this year (775 companies), following a decade of decline, alongside the continued dominance of the enterprise software segment among newly established companies.

The effects of artificial intelligence are not limited solely to enterprise software companies. Growth can also be seen in investments in companies across all fields that are developing solutions at the core of AI, from vertical models (Vertical AI) to enabling infrastructure in the worlds of chips and energy. The surge in demand for computing and chip infrastructures, which enable the AI revolution, may also explain part of the renewed growth in the hardware segment.

In terms of human capital, high-tech employs more than 400,000 people, with 2.5% employment growth in the sector, but the sector’s share of total employment in the economy remained almost unchanged. The number of R&D employees declined for the first time, while product roles grew significantly. This trend correlates with greater efficiency in development work supported by AI tools and the expansion of Israeli companies’ R&D departments outside Israel.

Alongside the strengths reflected in the report, several significant challenges for the future are also highlighted:

- Exposure to exchange rate fluctuations: The sector’s dependence on exports (about 80% of high-tech output), and on investments denominated in US dollars creates extreme high-tech sensitivity to fluctuations in the USD-NIS exchange rate. The decline in this exchange rate in 2025, and even more so in 2026, eroded companies’ profitability, as revenues remained dollar-based while salary and operating expenses remained shekel-denominated. This trend shortened the financial runway of many startups and led to a real increase in employment costs in Israel compared with alternatives abroad.

- Concentration of Fundraising: Fundraising amounts that were previously distributed among more than 900 companies are now concentrated in only about 500 funding rounds. This concentration has reduced the number of companies able to secure financing through equity investment. The impact is also reflected in the reduction in capital available to early-stage companies, as well as in the capital available to companies outside the cyber and enterprise software segments, where 55% of investments are concentrated.

- Expansion of operations abroad: Analysis of the six years examined (since 2019) reveals a consistent trend of Israeli companies expanding employment abroad. Beyond the expected growth in marketing, sales, and technical support departments, consistent growth was also recorded in core R&D roles and in the appointment of senior executive (C-Level) positions, primarily in the United States. This figure comes against the complex backdrop of 2023-2024, during which the number of high-tech professionals who left Israel for extended periods increased by more than 40% compared with 2022.

- The gap from the long-term trend: Despite growth in 2025, a gap of approximately NIS 19 billion still exists between current high-tech output and the expected growth trajectory had the pre-2023 trend continued uninterrupted.

In the coming years, the most critical questions for Israeli high-tech will focus on preserving the attractiveness of economic activity in Israel and on the sector’s ability to adapt to the rapid pace of change driven by the AI era and geopolitical developments. In this context, it will be necessary to assess whether the trends of expansion and relocation of activity abroad indicate a healthy process of maturation and globalization, or whether they constitute a warning sign that reflects a deliberate reduction of activity in Israel, and how these processes will affect the future of employment and ecosystem development in Israel. Ultimately, the major test will be whether Israeli high-tech can once again demonstrate the rapid structural agility that characterized it in the past, leading in the critical axes of technological value creation and rebuilding the “moat” of Israeli high-tech in the face of intense global competition.