Climate Tech Startups by Climate Challenge

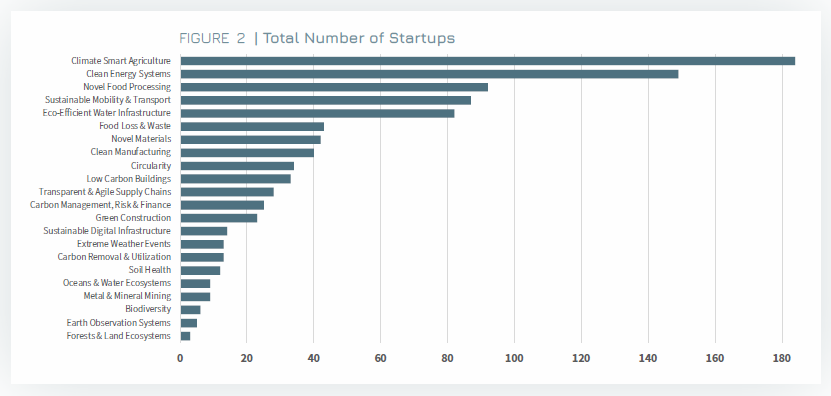

The updated mapping of Israeli climate tech startups identified a total of 946 startups offering solutions to climate challenges, reflecting steady growth in the ecosystem. This represents an increase of 162 startups compared to the 784 climate tech startups identified in 2023. Among these, 49 startups were founded since H2 of 2023. This number represents a decrease in the trend of new climate startups that could be explained, at least partly, by the geopolitical situation in Israel. Figure 2 illustrates the distribution of these startups based on the primary climate challenge they address.

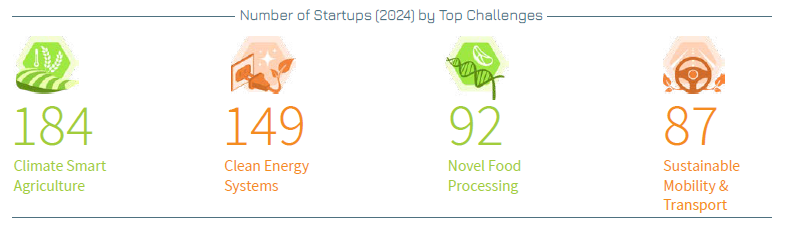

The five most prolific challenges addressed by startups remain consistent with those in the 2022 and 2023 Reports: Climate Smart Agriculture, Clean Energy Systems, Novel Food Processing, Sustainable Mobility & Transport and Eco-Efficient Water Infrastructure. These challenges are addressed by 184, 149, 92, 87 and 82 startups, respectively.

Despite the historical dominance of Climate Smart Agriculture and Clean Energy Systems challenges, new data reveals more balanced distribution of startups across these climate challenges. This shift suggests that entrepreneurs are increasingly exploring opportunities in a wider variety of fields, demonstrating greater openness to emerging sectors.

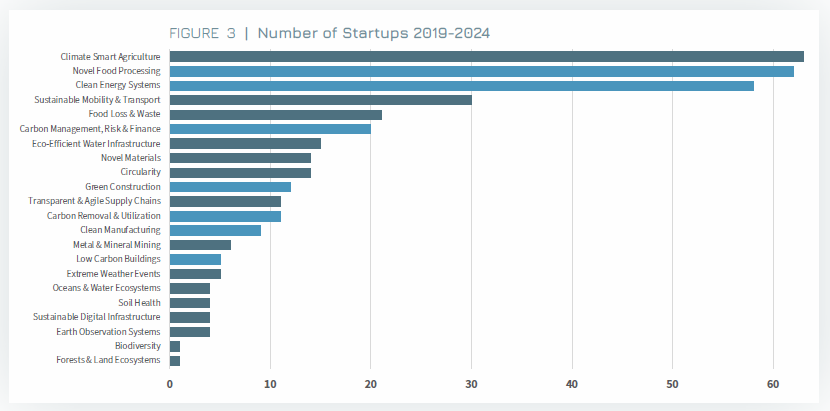

This trend is further illustrated by Figure 3, which maps startups established since 2019 (374 startups, representing 39.5% of the total). The darker shaded bars emphasize significant ranking shifts for newer startups compared to the full dataset. Notably that in this time period:

- Novel Food Processing challenge has overtaken Clean Energy Systems as the second most addressed challenge, with nearly the same number of startups as the top challenge Climate Smart Agriculture.

- Sustainable Mobility & Transport, while a well-established sector in Israel, is now ranked as number 4 of the most addressed challenges and accounts for only one-thirds of the new startups in the top challenge.

Additional changes in rankings compared to the 2023 Report include:

- Carbon Management, Risk & Finance saw the most significant rise, moving up six positions, reflecting a growing focus on startups addressing this challenge.

- Clean Manufacturing, Low Carbon Buildings and Sustainable Digital Infrastructure dropped five positions, indicating a relative decline in newer startups entering these fields.

- Carbon Removal & Utilization and Metal & Mineral Mining climbed four and five positions correspondently, while Eco-Efficient Water Infrastructure and Novel Materials dropped by two and three positions, continuing the trend observed in previous years.

These developments highlight the dynamic nature of the climate tech ecosystem, with emerging fields gaining traction and mature sectors consolidating their presence. The evolving focus of entrepreneurs underscores the importance of adapting strategies to support innovation across a broader range of climate challenges.

Among them, 6 startups in the Novel Food Processing sector raised a total of $4.5 million USD, while a standout Novel Materials company secured an impressive $8.7 million. While the rest are in different stages of raising funds.

This conclusion is further supported by the distribution of the 49 new startups founded in 2023-2024 and the primary challenges they address. The figure illustrates a relatively balanced distribution, with the largest share of 27% focused on Novel Food Processing, followed by 10% addressing the Climate Smart Agriculture and Food Loss & Waste challenges. Notably, almost 25% of these new startups have already secured VC and grants funding, collectively raising $15.36 million.

The Emergence of New Climate Tech Startups by Climate Challenge

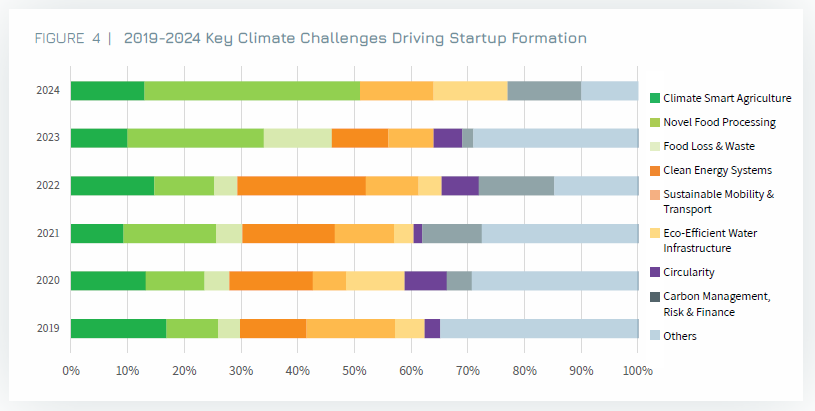

To gain deeper insights into the annual emergence of new climate technologies, we analyzed startups founded each year and mapped them according to their primary climate challenge. For the sake of consistency, methodological rigor, and ensuring comparability with previous years, we followed the format established in prior reports. Figure 4 highlights the eight challenges with the highest cumulative number of startups established during the period 2019–2024. These 8 challenges comprise between 63%-87% of all the startups established each year. The climate tech ecosystem in Israel continues to demonstrate dynamic shifts in the focus areas of new startups. Based on the latest data, the distribution of startups across key challenge areas has evolved significantly, reflecting both emerging opportunities and changing priorities within the sector.

The data reveals a clear trend toward prioritizing high-growth and emerging challenge areas, such as Novel Food Processing, Eco-Efficient Water Infrastructure, and Carbon Management, Risk & Finance. At the same time, traditionally dominant sectors like Clean Energy Systems and Climate Smart Agriculture are stabilizing, signaling a shift in entrepreneurial focus and market dynamics.

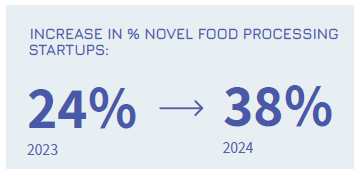

- Novel Food Processing: This sector now accounts for 38% of newly established climate tech startups in 2024, up from 24% in 2023 and 9% in 2019. While this growth reflects continued entrepreneurial activity and interest in sustainable food solutions, it does not necessarily translate into increased investment. Historically, the sector has attracted significant funding, but in recent years, investor confidence has weakened, leading to a decline in new capital inflows. Both globally and in Israel, alternative proteins have faced increasing financial pressures, with some companies struggling to scale, secure funding, or sustain operations.

Despite these challenges, innovation in the sector persists, with startups exploring new production methods, cost reductions, and improved scalability to regain momentum.

The sector’s current positioning reflects its strong foundation from previous investment cycles, but its future trajectory will depend on its ability to rebuild investor confidence and demonstrate sustainable market demand.

- Climate Smart Agriculture: Once a dominant area in earlier years, this sector has seen fluctuations in its share of new startups. While it accounted for 25% in 2018, Climate Smart Agriculture saw a drop to 9% in 2021 but rebounded to 13% in 2024. This consistent focus and renewed attention make sense, as agriculture remains a significant innovation market in Israel, aligning with the country’s strengths in agri-tech and its global reputation for advancements in sustainable agricultural solutions.

- Clean Energy Systems: After peaking at 23% of new startups in 2022, this sector experienced a sharp decline to 10% in 2023 and is now less dominant. While fewer new startups are entering this space, innovation remains strong among established players. Notably, most new startups in this sector are focused on hydrogen technologies, signaling a move toward breakthrough solutions in clean energy production, storage, and distribution. This shift highlights the evolving nature of the sector, with increasing emphasis on next-generation technologies rather than traditional renewable energy solutions.

- Sustainable Mobility & Transport: While this sector remains well-established, its share of new startups has stabilized at 13% in 2024, reflecting steady interest in addressing transportation-related emissions, with a particular focus on EV charging infrastructure and battery technologies.

- Eco-Efficient Water Infrastructure: A notable resurgence is observed in this sector, which now accounts for 13% of new startups in 2024 after being at 0% in 2023. This revival indicates renewed innovation in water technologies, likely driven by increasing concerns about water scarcity and efficiency.

- Carbon Management, Risk & Finance: After a brief decline to 2% in 2023, this sector has rebounded to 13% in 2024, highlighting growing interest in carbon tracking, risk management, and financial resilience solutions.

- Circularity: This challenge area has maintained a relatively small but steady share of new startups, accounting for 5% in 2023. Its fluctuations, from 8% in 2020 to 2% in 2021, suggest that innovation in this space remains sporadic but important.

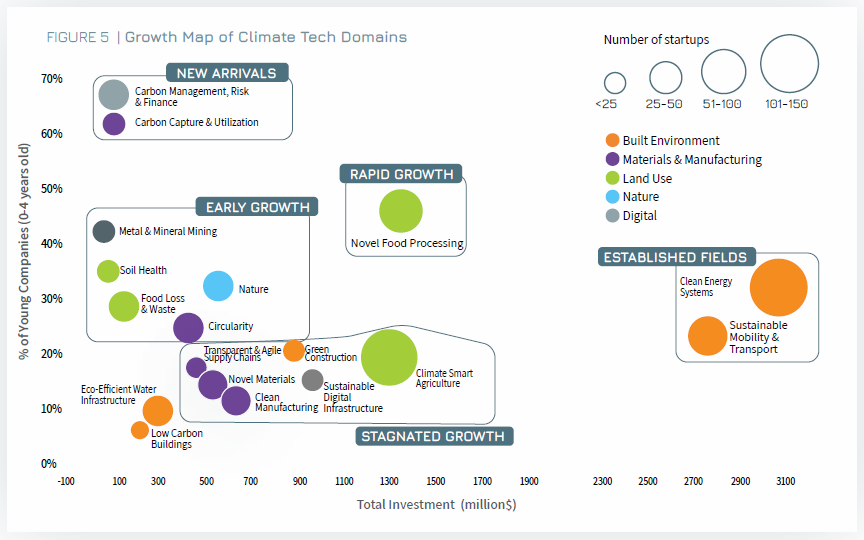

Growth Map of Climate Tech Domains

An analysis of startup growth rates by climate challenge reveals some significant shifts in 2024, as illustrated in Figure 5. The figure highlights the percentage of young startups (0 -4 years old), total known investments for each challenge, and the relative size of each challenge by the total number of startups. The challenges are grouped into distinct clusters based on common characteristics: Established Fields, Rapid Growth, Stagnated Growth, Early Growth, and New Arrivals.

Cluster 1: Established Fields includes two Challenges: Clean Energy Systems and Sustainable Mobility & Transport

These challenges continue to dominate the climate tech ecosystem, attracting the highest total investment and supporting a substantial number of startups. Clean Energy Systems and Sustainable Mobility & Transport maintain their positions as mature and well-established sectors, demonstrating steady funding and sustained growth. While new companies continue to enter these fields, their growth rates are slower compared to emerging sectors. Notably, the pace of new startup formation has declined in recent years, signaling a strategic shift in investment priorities—moving from early-stage ventures toward scaling infrastructure, commercialization, and large-scale deployment.

Cluster 2: Rapid Growth of Novel Food Processing

The sector continues to attract a high rate of young startups with a high rate of investments, thus reflecting strong entrepreneurial activity and sustained investor confidence. Its momentum has been shaped by past global demand for sustainable food alternatives and historically high investment in food tech R&D. While investment in alternative proteins has slowed in recent years, Israel remains a key player in the sector, leveraging its strong scientific foundation and innovation-driven ecosystem. The sector’s continued development will depend on its ability to overcome financial challenges, enhance scalability, and rebuild investor confidence, reinforcing its role in advancing sustainable food solutions and reducing the environmental impact of traditional protein production.

Cluster 3: Stagnated Growth with the following Challenges: Climate Smart Agriculture, Novel Materials, Clean Manufacturing, Sustainable Digital Infrastructure, Green Construction

The Stagnated Growth cluster includes challenges that, despite their importance to decarbonization, show a low proportion of newly founded startups:

- Climate Smart Agriculture: After years of being a leading challenge area, it has now entered stagnation, with the proportion of young startups dropping below 20%.

- Novel Materials and Transparent & Agile Supply Chains: These challenges moved into the Stagnated Growth cluster due to a sharp decline in new startups, falling to almost 10%. Interestingly, many of these companies emerged during a period of high interest before 2020, and this year’s 4-year filter excludes them, reflecting a slowdown in new activity.

- Clean Manufacturing, Green Construction and Sustainable Digital Infrastructure remain in this cluster, with limited startup formation and modest investment growth.

This stagnation signals both challenges and opportunities for these sectors. While mature companies continue to dominate, a lack of new entrants could hamper future innovation and investment momentum.

Cluster 4: Early Growth with the following Challenges: Food Loss & Waste, Circularity, Soil Health, and Nature

The Early Growth cluster consists of climate challenges that, while having fewer total startups, show strong potential for expansion due to a promising share of young companies and increasing early-stage investment. These sectors reflect growing entrepreneurial interest and alignment with global sustainability priorities.

- Metal & Mineral Mining has emerged as a focus area, driven by the rising demand for critical raw materials essential for clean technologies, particularly in battery supply chains.

- Soil Health is also gaining traction, with increasing attention on regenerative agriculture and carbon sequestration, attracting new startups working on sustainable land management solutions.

- Circularity and Food Loss & Waste continue to see steady startup formation, reflecting the growing focus on reducing inefficiencies in global food systems.

Similarly, Nature-Based Solutions are becoming more prominent, with a growing number of startups dedicated to biodiversity restoration, ecosystem services, and natural climate solutions.

The expansion of the Early Growth cluster indicates that entrepreneurs are targeting a broader range of climate challenges, particularly in resource efficiency, sustainable food systems, and biodiversity protection. While these sectors continue to develop, unlocking greater investment potential will be critical for their long-term growth and impact.

Cluster 5: New Arrivals with the following Challenges: Carbon Management, Risk & Finance, Carbon Capture & Utilization

The New Arrivals cluster remains centered around Carbon Management, Risk & Finance and Carbon Capture & Utilization, both of which continue to attract a high proportion of young startups (~70%). This trend underscores the sustained focus on carbon markets, emissions reduction, and risk management, as startups respond to tightening global regulations, corporate sustainability commitments, and evolving carbon pricing mechanisms.

These challenges represent emerging opportunities for both founders and investors, as they are still in the early stages of development but align with the global trends.

Low Carbon Buildings and Eco-Efficient Water Infrastructure continue to occupy the lower left quadrant of the graph, indicating that they have yet to attract substantial new investments or entrepreneurial activity.

Key Takeaways

The growth clusters highlight the dynamic nature of the climate tech ecosystem:

- Established fields such as Clean Energy Systems and Sustainable Mobility & Transport maintain their leadership but face slower relative growth.

- Rapid Growth is concentrated in Novel Food Processing, reflecting increasing demand for sustainable food solutions and good R&D base in Israel.

- Stagnation in challenges like Climate Smart Agriculture and Novel Materials points to a need for renewed innovation and investment in these fields.

- New and emerging challenges, such as Metal & Mineral Mining and Sustainable digital infrastructure, present promising opportunities with high entrepreneurial activity despite current low startup numbers.

These trends underscore the importance of supporting innovation across all clusters to ensure balanced growth and progress toward climate resilience and decarbonization.

Investments landscape

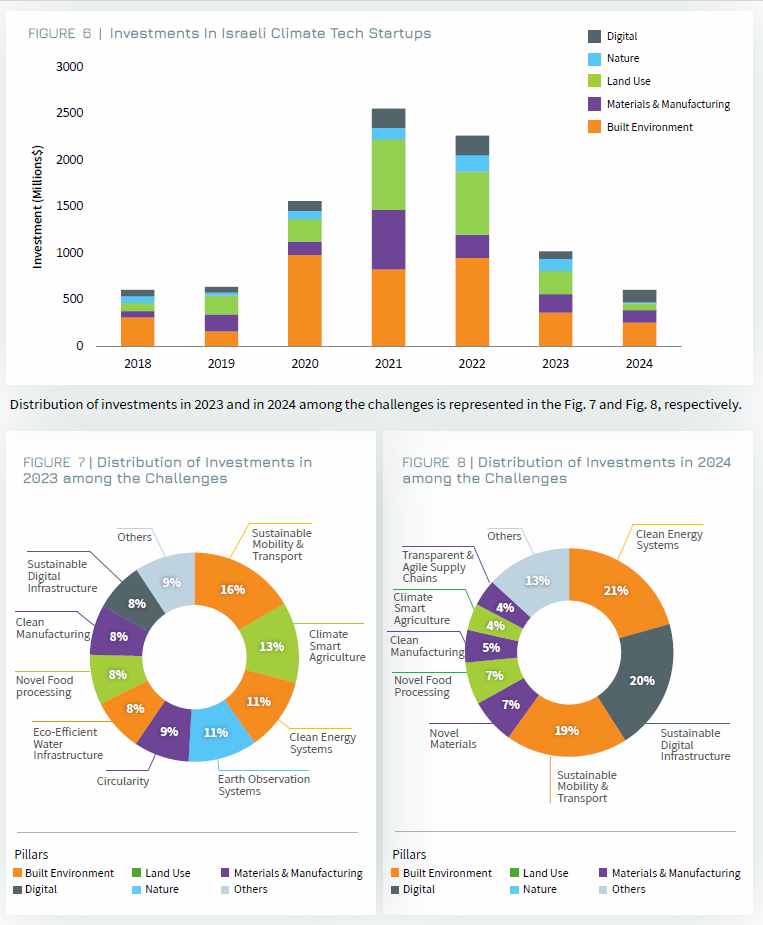

Investments in Israeli climate tech ventures totaled $9.5 billion between 2018 and 2024 (Figure 6). In 2023, climate tech investments reached $1 billion, a decline of 51% from the $2.27 billion recorded in 2022. Despite the challenging economic climate and the ongoing geopolitical circumstances in Israel, climate tech demonstrated notable resilience. Encouragingly, H2 2023 investment levels remained close to those of H1 2023, and investments in 2024 totaled $613million, reinforcing the sector’s ability to attract capital and maintain momentum despite broader market challenges.

The significant increase in investments in Sustainable Digital Infrastructure can be attributed to the rising demand for energy-efficient solutions, data center cooling technologies, and computational optimization, driven by the rapid growth in AI applications.

While climate tech investments in Israel declined from $2.27 billion in 2022 to $1 billion in 2023 and further to $613 million in 2024, overall early and growth-stage investments in Israel fell in similar percentage from $15.9 billion in 2022 to $6.9 billion in 2023, before rebounding to $9.6 billion in 2024. We expect to see a rebound back of investments also in Climate tech in 2025, given the flourishing activities of the ecosystem and presence of investors, later discussed in this chapter.

Despite this downturn, climate tech demonstrated notable resilience within Israel’s tech ecosystem. In 2023, climate tech accounted for 14.5% of total tech investments, up from 14.3% in 2022, highlighting its resilience despite economic and geopolitical challenges. In 2024, climate tech’s share adjusted to 6.4%, reflecting a shift in investor priorities but still maintaining a significant presence. At the same time, we anticipate 2025 to be a stronger year for Israel’s climate tech sector, driven by an improving global investment climate and the sector’s proven ability to outpace other industries during periods of economic recovery. Historically, climate tech has demonstrated higher growth rates in the expansion phases of the economic cycle, positioning it well for renewed investor interest and accelerated development.

The decline in Israeli climate tech investments in 2023 and 2024 aligns with global trends, though it has been more pronounced than in other markets. In the U.S., capital raised for climate tech-focused VC funds declined from $59 billion in 2022 to $44 billion in 2023, a 25.4% drop, with 2024 numbers showing relative stability. While Israel experienced a sharper contraction, the sector’s resilience within the broader tech downturn underscores its long-term potential to attract investment and drive innovation in climate solutions.

Investor Landscape

Israeli climate tech continues to attract significant international investment, reinforcing its position as a global hub for climate innovation. Historically, a large share of funding has come from international investors, with the U.S playing a leading role in financing Israeli climate startups.

In 2023, there were 135 investment rounds, and in 2024, there were 90 rounds across various climate tech sectors. Notably, in over 90% of these rounds, multiple international investors participated, demonstrating strong global confidence in Israel’s climate tech ecosystem.

Venture capital remains the dominant funding source, with a balanced distribution between Israeli and foreign VCs. However, corporate venture capital investments predominantly come from international entities, reflecting the global demand for Israeli climate solutions. Private investors, many of whom originate outside of Israel, have also played a key role in supporting early-stage startups.

Despite economic challenges, the continued engagement of international investors highlights the resilience and attractiveness of Israeli climate tech. As the sector matures, global partnerships will remain crucial in scaling innovation, fostering commercialization, and driving the next wave of climate solutions.

Funding Stage of Climate Tech Startups

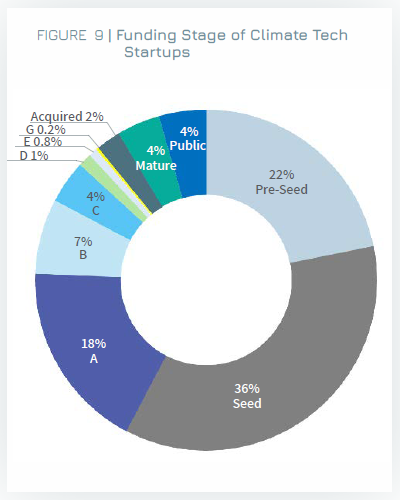

The funding stages of Israeli climate tech startups are detailed in Figure 9, reflecting the ecosystem’s growth dynamics and investment patterns. In 2024, the majority of startups are still in the early fundraising stages, with 36% at the Seed stage and 22% at the Pre-Seed stage, collectively accounting for 58% of all funded startups. This aligns with the observation that most companies are relatively young, supporting the continued influx of early-stage investment.

Progression beyond Series A demonstrates significant growth potential, with 18% at Series A and 7% at Series B, indicating a promising pipeline of startups ready to scale. As 4% have reached Series C and 0.8% have advanced to Series E, the ecosystem shows early signs of maturity, paving the way for future growth and expansion opportunities. Notably, Series G is represented by 0.2%, highlighting the emerging potential for large-scale growth financing. This distribution reflects a dynamic and evolving investment landscape, with substantial opportunities for investors to support the next wave of climate tech leaders.

In terms of exits and maturity, 4% of companies are publicly traded, while 4% are categorized as mature, and 2% have been acquired. These figures indicate modest exit activity, consistent with the ecosystem’s overall youthful profile.

As a testament is the growing investor landscape active in the Israeli climate-tech ecosystem, with over 50 Venture Capital firms (VC’s) and a handful of family offices specializing in climate technologies compared to under 10 active VC’s in 2021. Foreign investors are also increasingly active, with at least 10 international VCs making multiple investments in Israeli climate tech startups in 2024. Corporate venture capital (CVC) plays a significant role, with at least 10 CVCs focused on climate innovation, such as Microsoft, Volkswagen Group, Doral Energy-Tech Ventures, and Ormat. Investment activity has remained strong, with at least 25 high-value rounds (>$10million) recorded in 2023 and 14 in 2024, and an increasing activity of early-stage deep tech companies backed by technology incubators funded by the Israel Innovation Authority.

We can characterize Israeli climate tech investments as having developed rapidly since 2018, initially outpacing global growth rates. However, since 2021, Israeli climate tech investments have mirrored global trends more closely. This shift may signal the mainstreaming of the market, as climate tech becomes increasingly integrated into the broader technology and investment landscape.

Overall, the Israeli climate tech sector continues to demonstrate remarkable resilience, maintaining investor interest and growing its share of national tech investments. The sector’s steady performance, coupled with significant investment in emerging areas like Sustainable Digital Infrastructure and Novel Food Processing highlights its critical role in driving innovation and supporting global climate goals.