Introduction

Throughout 2024, the global and Israeli trend of declining investments in the FoodTech sector continued – the process began in 2022 following record fundraising levels in 2021. The data on the volume of global investments is still incomplete, but forecasts indicate a problematic year for the sector. According to the DigitalFoodLab website, investments in the field totaled approximately $8 billion in the first half of 2024. However, a breakdown of these investments by category reveals that the term “FoodTech” also includes areas such as ConsumerTech, Foodservice, and AgTech, which are not directly related to food and food ingredient development. In contrast, the more relevant field – Food Science, which includes the alternative protein category – constitutes only about a quarter, or roughly $2 billion, of the total investment within the broader category. The same source predicts that the total investment sum for all of 2024 will be similar to that of 2023.

Investments in Food Science have not constituted the majority within what research firms define as the FoodTech sector over the past decade. The “Delivery” category has typically dominated investment allocations, mostly encompassing online grocery delivery applications. Additionally, in most research firm reports, the AgTech sector is included under FoodTech; however, it is a distinct domain. AgTech companies focus on pre-harvest products and technologies; therefore, their relevance to FoodTech technologies, mostly post-harvest, is limited.

The decline in FoodTech investments, continuing into 2024, is summarized in an article published on Foodnavigator.com, which is based on insights from several venture capital representatives. The main points are that the investment downturn is expected to worsen into 2024, as venture capital funds face challenges raising capital and have become more selective in choosing startup investments. Already, a significant number of FoodTech companies are fading due to their inability to secure funding, and according to the article’s authors, this trend is expected to continue in the coming years. There has also been a notable decrease in investments in FoodTech companies operating in areas related to ClimateTech (such as alternative proteins). Many generalist investors who entered the field driven by hype, without fully understanding the broader picture, have exited. Specialized investors continue to invest actively, but in a more discerning manner.

According to the article, the trend among investors in the FoodTech sector over the past two years has been to invest in companies developing innovative B2B food ingredients (as opposed to companies developing final food products) and in technologies that are expected to drive growth in the field (enablers – companies focused on addressing taste, texture, and nutritional aspects of meat and dairy alternatives, as well as those developing scale-up solutions for biotechnological food production). In addition, investors tend to favor companies with leaner structures that require less reliance on capital infusions from venture capital funds.

The article concludes with an optimistic outlook for the Food Tech sector – a gradual recovery and renewed growth in investment volume, expected to reach approximately $6 billion in 2025 and close to $8 billion in 2026. However, the sector now requires patience and “smart money” – investors can no longer expect the same returns or exit timelines commonly seen in the FinTech or software sectors.

State of FoodTech Investments in Israel

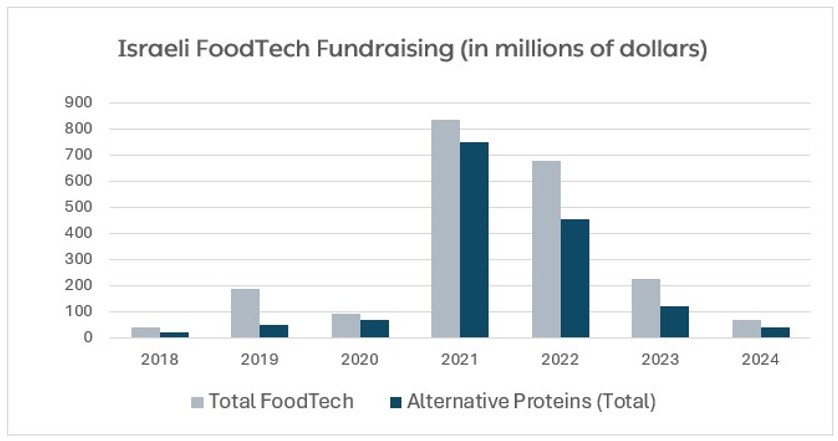

The current state of capital raising in the Israeli FoodTech sector reflects a significant decline of approximately 60% compared to 2023, which was already a challenging year for the industry. Total fundraising in the field amounted to around $66 million, with approximately $40 million directed toward developing alternative proteins (Figure 1). According to the final report by Startup Nation Central and additional analyses, Israeli FoodTech fundraising in 2024 totaled around $88 million. However, this sum includes fundraising by companies irrelevant to this review; therefore, the graphs do not present these figures. This review excludes fundraising by companies developing digital applications, products, or technologies in the AgTech domain.

Figure 1: Total Investments and Fundraising in Israeli FoodTech

Source: Analysis of data from Startup Nation Central and Israel Innovation Authority

Compared to the global trend in FoodTech fundraising in 2024, Israel’s investment volume decline has been significantly steeper.

According to reports from Israeli startups, one of the main reasons is the geopolitical situation following the “Iron Swords” war, which led to the cancellation or postponement of planned funding rounds, primarily by foreign investors who refrained from entering new investments. Although the impact is not unique to the FoodTech sector, when combined with the increased selectivity of investors in this field globally, the consequences for the industry in Israel have been particularly severe.

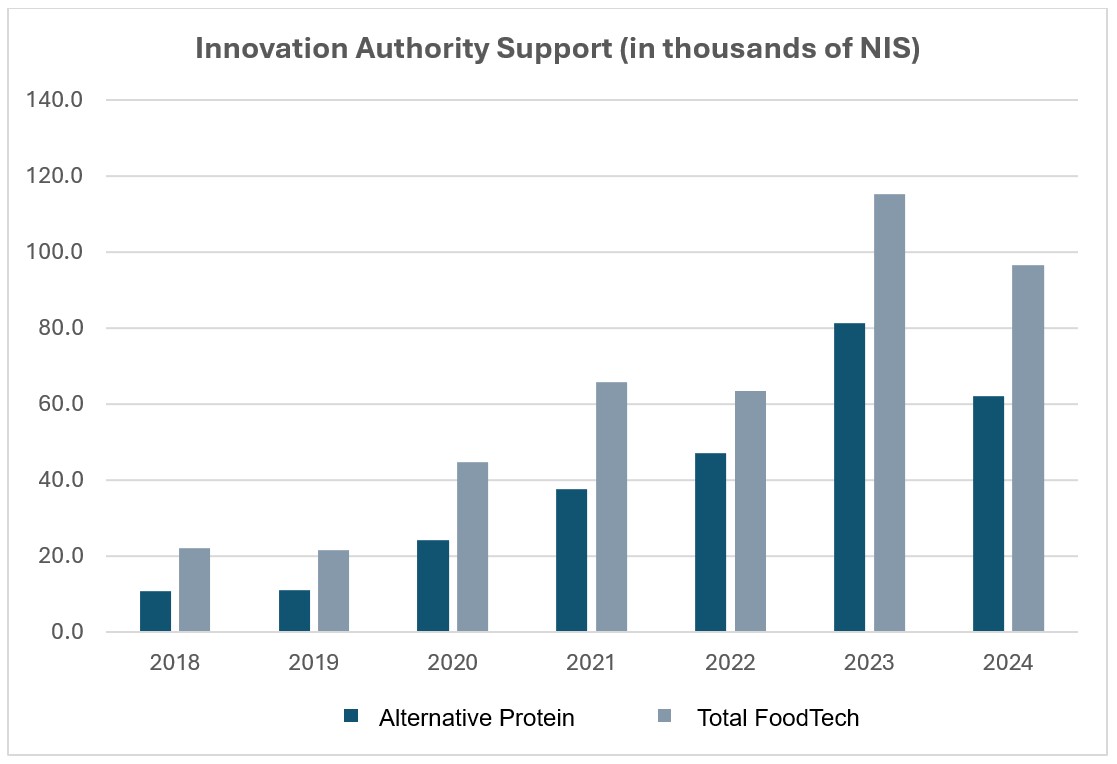

Scope of Israel Innovation Authority Support for the FoodTech Sector in 2024

Scope of Israel Innovation Authority Support for the FoodTech Sector in 2024

In 2024, the Authority supported 50 companies and entrepreneurs in the field. This figure is slightly lower than the support provided in 2023 but still reflects a significant activity level in a challenging year for the sector (Figure 2).

As part of its support for FoodTech, the Authority provided considerable backing for the alternative protein sector: more than 43% of the support in this category was directed toward plant-based protein, approximately 38% toward fermentation-based programs, and about 19% toward cultivated meat initiatives.

Figure 2: Israel Innovation Authority Support for the Israeli FoodTech Ecosystem Over the Years

Source: Analysis based on data from the Israel Innovation Authority

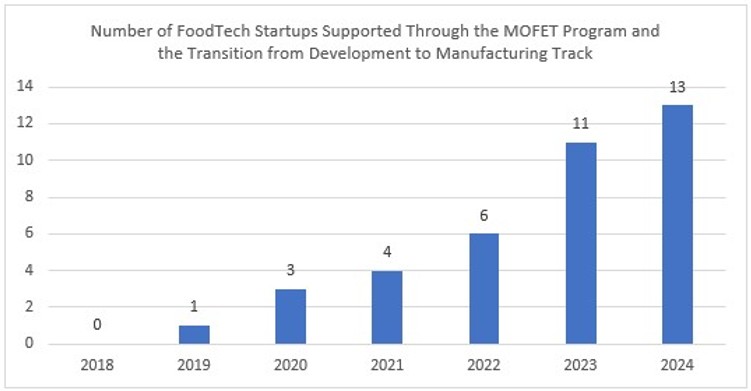

In parallel, the upward trend continues in the number of FoodTech companies applying through advanced manufacturing tracks – the MOFET Program and the Transition from Development to Manufacturing track (Figure 3). This positive trend is expected to lead at least some of these companies toward commercialization and local production in Israel.

Number of FoodTech Startups Supported Through Advanced Manufacturing Tracks

Figure 3: Number of FoodTech Companies Supported Through Advanced Manufacturing Tracks Over the Past Seven Years

Source: Analysis based on data from the Israel Innovation Authority

As part of the continued increase in FoodTech support, the following provides an updated snapshot of Israeli FoodTech companies and their areas of activity (Table 1). The list includes 32 companies, most of which have received support from the Israel Innovation Authority.

Table 1: Israeli FoodTech Companies in Pilot and Sales Stages

| Company | Year Established | Sector |

|---|---|---|

| BioHarvest | 2007 | Biotechnology platform for producing dietary supplements and functional food from plant cells. Flagship product: VINIA – red grape cell powder intended for integration in food and beverage products |

| Innovopro | 2013 | Platform for chickpea protein extraction. The flagship product is a non-allergenic chickpea protein concentrate with broad potential for food industry applications |

| Incredo (DouxMatok) | 2014 | Sugar reduction solution (sugar-based). The company’s solution enhances sweetness perception without aftertaste, enabling significant sugar reduction in chocolate, cakes, biscuits, caramel, spreads, gummies, and more |

| Simpliigood (Algeacore) | 2015 | Cultivation and development of spirulina-based products. Specializes in developing fish and meat alternatives made entirely from spirulina using proprietary technology to neutralize the green color and create a fibrous texture |

| Panda Chocolate | 2015 | Production and development of vegan chocolate products replicating the quality of milk chocolate |

| Supermeat | 2015 | Development of cultured chicken meat. Focused on developing and producing chicken products through sustainable cell cultivation |

| Solato | 2015 | Machines and capsules rapidly prepare ice cream, sorbet, and frozen yogurt. On-site production reduces 85% of the energy typically required for industrial production, transport, and storage |

| Bravel | 2016 | Microalgae-based protein for dairy, meat, and egg alternatives. Technology combines sugar-based fermentation and high-intensity light to produce affordable microalgae |

| Amai Proteins | 2016 | Developing high-intensity protein sweeteners enables a 40-70% reduction in sugar in foods and beverages. Based on a protein design platform for high processing stability and sweetness 3,000 times stronger than sugar. Produced via microbial fermentation |

| Vgarden | 2017 | Develops, manufactures, and markets plant-based meat and dairy alternatives |

| Better Juice | 2017 | Reduces sugar in fruit juice by converting it into dietary fiber without altering taste or aroma. Technology relies on non-GMO microorganisms and continuous bioconversion to process large juice volumes with minimal cost impact |

| Redefine Meat | 2018 | Development and production of meat alternatives using additive manufacturing (3D printing). Proprietary technology, software, and formulations create a meat-like appearance, texture, taste, and properties |

| Savoreat | 2018 | A robotic ‘chef’ that produces and grills meat alternatives based on user preferences. Products mimic the appearance, texture, and taste of animal-based originals |

| Gavan Technologies | 2018 | Multi-purpose alternative to animal fat and fat in general, based on plant protein. Proprietary extraction platform isolates natural plant proteins in their native form |

| Sufresca | 2018 | Natural edible coating for fruits and vegetables to extend shelf life, reduce food waste, and plastic packaging |

| Remilk | 2019 | Animal-free dairy products. Uses microbial fermentation to produce and replicate milk proteins with the same taste, texture, and nutritional profile as traditional dairy |

| Torr Foodtech | 2019 | Snacks made from 100% natural ingredients without additives for bonding or preservation. Eliminates the need for sugars used to bind and stabilize snacks; offers high nutritional value |

| Kinoko Tech | 2019 | Natural mushroom-based food products. Developed a biological fermentation process using legumes and grains with mushrooms to create tasty, high-protein, nutrient-dense foods |

| Anina Culinary Art | 2020 | Quick-preparation meals are designed as capsules made from vegetables and natural ingredients. Produced from fresh agricultural produce, combining aesthetics, taste, nutrition, and convenience |

| Chunk Foods | 2020 | Plant-based meat alternatives in whole-cut style. Technology enables high-scale production, realistic meat appearance, and substantial nutritional value |

| Yo! Egg | 2020 | Plant-based egg alternative. The company’s products are designed as sunny-side-up eggs made from plant-based ingredients, targeting consumers who seek to avoid harm to animals and the environment, without compromising on the appearance, taste, texture, or nutritional values of a sunny-side-up or poached egg. |

| Blue Tree | 2020 | Technology platform for sugar reduction in juices and natural beverages. Selectively removes sugar without adding non-native ingredients or changing beverage composition |

| Vanilla Vida | 2020 | Revolutionizing vanilla cultivation and supply chain. Developed controlled growth and accelerated ripening technology for high-quality commercial vanilla pods |

| Imagindairy | 2020 | Animal-free dairy products using precision fermentation. The technology core is based on computational and molecular biology to enhance milk protein expression in microorganisms |

| Maolac | 2021 | Production and development of functional proteins for food, supplements, and cosmetics. Uses a proprietary proteomics-based computational platform to identify functional proteins |

| Oshi | 2021 | Plant-based fish and seafood alternatives. Produces whole-cut fish fillets using additive manufacturing, enabling low-cost industrial-scale production |

| Alfred’s Food-Tech | 2021 | Plant-based meat and dairy alternatives. Technology platform reduces off-flavors, allows high protein content, and enables large-scale production |

| Egg-n-Up | 2021 | Plant-based egg alternatives for food industry applications. Clean-label, functional, and cost-effective |

| Phytolon | 2021 | Natural food colorants. Yeast fermentation platform enables production of a wide range of stable, low-cost natural colors for food processing, replacing synthetic colorants |

| ProLeafEra | 2021 | Clean process platform for isolating plant protein from leaves. Avoids green color, bitter taste, and odors. Aims to support clean, sustainable agriculture and reduce carbon footprint |

| Exosomm | 2021 | Milk-derived exosome-based nutritional solutions. Develops patented immune-support supplements based on a proprietary proteomics platform |

| O’Taste | 2022 | Products for reducing sugar and sodium in food. Micronization technology shrinks the particle size of sugar and salt to enhance perceived sweetness/saltiness, allowing significant reduction without artificial additives |

Source: Company descriptions are based on information from the Startup Nation Central website and publicly available company data.

Developments in Regulation and Food Security

Regulation:

The upward trend continues in companies submitting applications for plant cell cultivation in bioreactors to produce food ingredients such as cocoa, coffee, antioxidants, pigments, and other natural compounds. In parallel, there is an increase in companies developing dedicated bioreactors for this technology. This field is gaining growing attention from international investors, including chocolate giant Mondelez which invested for the second time in the Israeli startup Bio Celleste, and the U.S. Department of Defense, which supports the development of these technologies alongside precision fermentation technologies.

In December 2024, the National Food Service at the Ministry of Health published a dedicated guidance document for FoodTech companies seeking marketing approval for products such as cultured meat and food ingredients and additives produced through precision fermentation. This guide was the primary goal of a joint pilot by the Israel Innovation Authority and the Ministry of Health, aimed at making the regulations, requirements, and process structure accessible for submitting applications related to alternative proteins and biotechnologically produced food.

The pilot included four companies in the alternative protein field and served as a regulatory “sandbox” for the Ministry of Health’s learning process in handling “novel food” approval requests for innovative products in the cultured meat and precision fermentation domains – fields that have been considered regulatory challenges both in Israel and globally. Two of the four companies received “novel food” approval as part of the pilot: Aleph Farms (cultured meat) and Remilk (milk proteins produced via precision fermentation).

In this context, it is noteworthy that in November 2024, the Ministry of Health also approved marketing the milk proteins developed by the precision fermentation company Imagindairy.

In this context, it is noteworthy that in November 2024, the Ministry of Health also approved marketing the milk proteins developed by the precision fermentation company Imagindairy.

Food Security:

Food security has become more central in Israel’s national strategic outlook. This importance has been amplified by supply chain disruptions during the COVID-19 pandemic and by the geopolitical situation following the “Iron Swords” war, both of which exposed Israel’s significant dependence on food and agricultural imports. In response to these challenges, the Ministry of Agriculture renamed itself the “Ministry of Agriculture and Food Security,” expanding its focus across the entire Israeli AgriFood value chain. “The National Food Security Program 2050” was formulated within this framework. Its interim outputs were published: six working groups addressed various aspects of food security, including: composition of the national food basket and consumption habits, local agricultural production, trade and international cooperation, the food industry, R&D and innovation, and food loss. These groups identified key challenges and barriers and examined potential solutions to support forming a national food security plan for Israel that ensures a consistent supply of fresh, healthy food during routine and emergencies.

Key Challenges and Focus Areas:

The Food Industry Working Group examined ways to strengthen local healthy and affordable food production while integrating innovative technologies. The main challenges identified include dependence on imported raw materials, high production costs, and low growth in new food manufacturing plants. Proposed directions for action include shifting the product mix toward healthier and more sustainable options, encouraging the development of Israel’s FoodTech industry, and improving supply chains to reduce costs and increase production efficiency.

The R&D and Innovation Working Group addressed approaches to technological innovation in agriculture and the food industry, emphasizing the development of an advanced research ecosystem to respond to emerging challenges and risks. Key directions include strengthening the connection between research, academia, and industry; promoting entrepreneurship in AgriTech, FoodTech, and aquaculture; establishing innovative food manufacturing plants; developing research and knowledge infrastructure; identifying sub-sectors with productivity gaps; and creating tools for prioritizing government support to align with the national food basket. Emphasis was also placed on transitioning from R&D to production and supporting advanced agriculture development.

The Food Loss Working Group presented alarming data showing that 37% of food produced in Israel is lost, amounting to over 23 billion NIS annually. The group set a goal to reduce food waste and loss at the source and across the different segments of the value chain, including addressing surpluses and waste (prevention of landfill disposal).

Summary

The year 2024 marked a five-year low in FoodTech fundraising, both globally and in Israel, with the Israeli ecosystem experiencing a significantly sharper decline, mainly due to the geopolitical impact of the “Iron Swords” war. Alternative protein remains the primary focus of investment, though it accounted for just over half of the total funding in Israel, in contrast to 90% and 66% in 2021 and 2022, respectively. The cultivated meat sector continues to struggle with doubts regarding its suitability and future as a viable alternative to conventional meat, as reflected in both funding trends and a wave of critical media coverage throughout the past year. Current investments in this field are highly selective, focusing on companies addressing at least one of the core techno-economic challenges, such as cell division rate, cell density, reduction of growth medium costs, and novel bioreactor technologies.

Reducing animal-based food consumption remains a global challenge, primarily due to environmental impacts and rising food demand. However, significant barriers to substitution remain technological. The “National Food Security Program 2050” published by the Ministry of Agriculture and Food Security aligns with this need. It promotes the development of innovative food production and agricultural methods while aiming to reduce dependence on imports.

In contrast to the decline in private fundraising, support from the Israel Innovation Authority for the Israeli FoodTech ecosystem remained stable in 2024, at levels similar to 2023, a year that marked the Authority’s highest grant volume. There is cautious optimism regarding renewed investment activity in 2025, although a return to the 2021-2022 funding levels is not expected.

- The information presented on external websites referenced in this report is the sole responsibility of those websites, and the Israel Innovation Authority bears no responsibility for it.

- Third parties provided some of this article’s details, information, and data; the Authority does not commit to their accuracy.

- This article contains links to external websites. The Authority has no control over the information, details, or data presented on these sites, and such references should not be interpreted as a recommendation, endorsement, or preference for the content, information, or services published on them. The Authority assumes no responsibility for the content of these websites or reliance on the information they provide.