Introduction

Healthcare systems worldwide face growing challenges, with one of the most pressing being the shortage of medical personnel. This phenomenon is widespread across many countries, including those in the European Union, the United States, and Canada, and is expected to intensify in the coming decades. The shortage is reflected in the widening gap between available positions and actual staffing, as well as in the low number of medical graduates relative to system needs. Peripheral regions are more affected than urban centers. The most impacted fields include family medicine, advanced surgery, mental health, geriatrics, nursing, and paramedical services such as physiotherapy and occupational therapy.

Despite a general increase in the employment of healthcare workers, the data show a growing workload, an aging medical workforce, declining enrollment in nursing and medical professions, and an uneven geographic distribution of professionals.

All indicators point to an urgent need for solutions: expanding the scope of medical support roles alongside the adoption of breakthrough technological innovation. The integration of artificial intelligence (AI) tools in healthcare can streamline processes and improve the quality of care. A policy combining workforce expansion with advanced technologies can transform the challenge into an opportunity – creating a stronger, more flexible, and innovative healthcare system.

![]()

Technologies in the Field

As the global shortage of medical personnel continues to grow, AI tools are emerging as a key part of the solution. AI-based technological solutions can be positioned along a spectrum ranging from full autonomy to decision-support tools:

Autonomous Decision-Making Technologies

(Decision Making, או Human-out-of-the-loop)

These technologies eliminate the need for physicians in specific fields or altogether, enabling complete automation. Examples include predicting clinical trial outcomes through AI-based medical data analysis, as well as automated alerts for patient monitoring and escalation detection, and automated diagnostics.

Decision-Support Technologies

(Decision Support Systems, או Human-in/on-the-loop)

These tools assist physicians and streamline their workflow, reducing the time required per patient. Examples include personalized medicine through clinical data analysis for tailored treatment, medical document transcription, and administrative support.

Currently, most AI tools in healthcare systems worldwide serve as decision-support systems, with limited autonomy that does not address the workforce shortage. However, a growing number of companies are developing technologies that can operate autonomously to some extent and perform specific medical tasks traditionally carried out by healthcare staff.

![]()

Leading Companies in the Field

The integration of AI in healthcare – driven by the need to address physician shortages and improve medical efficiency – has reached the world’s largest technology companies, including Alphabet, NVIDIA, and IBM. These corporations are investing substantial resources in the field, with some even establishing dedicated healthcare divisions. Their advantages include access to multidisciplinary talent, extensive existing knowledge bases, and independence from external hardware suppliers (for instance, NVIDIA manufactures its own chips for its products).

![]() Google Health – the digital health R&D division of Alphabet. Its goals include addressing physician shortages and improving accessibility to medical imaging and diagnostics. Notable AI developments include:

Google Health – the digital health R&D division of Alphabet. Its goals include addressing physician shortages and improving accessibility to medical imaging and diagnostics. Notable AI developments include:

- MedLM – AI models that assist physicians in complex research and in summarizing doctor-patient encounters.

- ARDA – system for diagnosing diabetic retinopathy.

- HeAR AI – analyzes vocal signals such as coughing, speech, and breathing to detect diseases.

![]() Nvidia established Nvidia Clara, a suite of AI-based healthcare technologies. Clara’s focus is on software rather than medical devices, and its developments include:

Nvidia established Nvidia Clara, a suite of AI-based healthcare technologies. Clara’s focus is on software rather than medical devices, and its developments include:

- Clara Deploy – a system for deploying and managing AI healthcare applications, enabling integration into clinical workflows.

- Clara Imaging – tools for developing AI applications for medical imaging.

![]() Amazon – leverages NLP and Generative AI technologies to help healthcare organizations analyze unstructured clinical text, extract critical information such as diagnoses and medications, transcribe doctor-patient conversations in real time, and structure medical data to generate insights. Amazon also provides services to other healthcare companies, such as Medhost.

Amazon – leverages NLP and Generative AI technologies to help healthcare organizations analyze unstructured clinical text, extract critical information such as diagnoses and medications, transcribe doctor-patient conversations in real time, and structure medical data to generate insights. Amazon also provides services to other healthcare companies, such as Medhost.

In addition to the major companies, which develop across sectors beyond medicine, the following are examples of notable companies specializing in healthcare and active in automation in health (listed in descending order of revenue):

| Company Name | Healthcare Automation | FDA Approvals | Users | Revenue 2024 (PitchBook) |

|---|---|---|---|---|

| Siemens – Germany | AI-based image analysis; robotic and AI-assisted blood testing; a system for recommending personalized treatment pathways | 69 approvals. Example: quantification and imaging of arterial calcification | Thousands of hospitals worldwide | USD 24.2B |

| GE – USA | Improving clinical outcomes through AI-based imaging, real-time monitoring, and decision support | 71 approvals. Example: image reconstruction algorithm enhancing scan quality | Dozens of hospitals in the US and UK | USD 19.7B |

| Philips – Netherlands | Production of AI-powered imaging machines for faster and more accurate scans | 24 approvals. Example: AI-integrated ultrasound | Hospitals worldwide | USD 800M |

Alongside developments by leading companies in the field, additional solutions are being explored to support the integration of AI in healthcare. These initiatives combine the efforts of companies, academia, hospitals, and governments in various ways to enable efficient AI adoption and address regulatory challenges in the sector.

![]()

Regulatory Sandboxes in AI and Healthcare

One of the key barriers to integrating AI in healthcare is regulatory, stemming from the need to balance patient safety with the ability to conduct research and develop innovative technologies. A standard tool used by governments worldwide to address this challenge is the regulatory sandbox. This framework allows for the controlled testing of new technologies, their gradual integration into medical systems, and the development of regulatory responses that support large-scale implementation.

In recent years, regulatory sandboxes for testing, piloting, and deploying AI tools in healthcare have proliferated globally. In the United Kingdom, AI Airlock focuses on regulatory alignment for AI-based medical devices through collaboration with government bodies. In the European Union, AI-Mind accelerates dementia diagnosis using AI, while AI DReAM in France focuses on medical imaging and developing a collaborative infrastructure for AI solutions. Additionally, the global initiative MONAI, developed and promoted by NVIDIA, provides an open-source framework for advancing medical AI, inviting contributions from researchers and developers.

Other sandboxes in countries such as Denmark, France, Sweden, and Germany primarily address regulatory challenges related to data privacy and the GDPR, often providing regulatory guidance but without legal exemptions or technical support.

While these models differ in maturity, funding, and oversight mechanisms, they share a common goal: to establish safe, flexible, and transparent frameworks for AI development and implementation, reducing regulatory barriers and providing clarity for developers, healthcare providers, and policymakers.

The following table summarizes and compares the various regulatory sandboxes:

| Sandbox | Focus Area | Objective | Regulatory Framework | Key Projects | Main Participants | Funding | Unique Features |

|---|---|---|---|---|---|---|---|

| AI Airlock (UK) | AI-based medical devices | Balancing regulation and innovation | UK Regulation (MHRA) | Improving LLM systems; personalized cancer programs; synthetic data for reports; real-time monitoring | MHRA, NHS, regulatory agencies | Government and self-funding | Integration of regulatory and clinical bodies; strict screening process; focus on adaptive models |

| AI-Mind (EU) | Early dementia diagnosis | Reducing diagnostic time to one week | Compliance with the EU AI Act | Detecting dementia markers in imaging, predicting disease risk | Hospitals, universities, companies, regulators | €14M from the European Commission | Multidimensional data integration; nine work-package structure |

| AI DReAM (France) | Medical imaging | Improving diagnosis and accelerating AI integration in healthcare | Not specified | Liver cancer, COVID-19, brain tumors, oncology monitoring | Startups, research labs, clinical centers | €13M from the French government | Openness to third-party development; accelerated regulatory registration |

| MONAI (Global) | Medical imaging (open source) | Bridging imaging research stakeholders | No formal regulation | Imaging model development, image labeling, and model deployment in clinical settings | NVIDIA, academia, healthcare institutions (NIH) | Not specified | Accelerated product launch; early-stage implementation |

| AI Sandbox (Denmark) | AI projects | Supporting GDPR-compliant initiatives | GDPR compliance | No healthcare projects included | Danish Data Protection Agency, Danish Agency for Digitisation | No funding | Legal (non-exempt) and regulatory support; no infrastructure or funding |

| AI for Public Services (France) | AI applications for public services | Promoting public-sector AI while protecting privacy | GDPR compliance | Previously addressed digital health | CNIL, public-sector experts | No funding | Regulatory guidance; no infrastructure, funding, or legal exemptions |

| AI Sandbox (Germany) | Cross-sector regulation | Encouraging regulatory innovation | Not specified | Unknown if healthcare projects are included | Federal Ministry for Economic Affairs (BMWE), Regulatory Sandbox Network | Not specified | Temporary regulatory exemptions; links between government and private entities |

| AI Sandbox (Sweden) | Generative AI | Evaluating GenAI for public document management | GDPR, Data Protection Act | Unknown if healthcare projects are included | Swedish Data Protection Authority (IMY) | Not specified | Provides legal support |

![]()

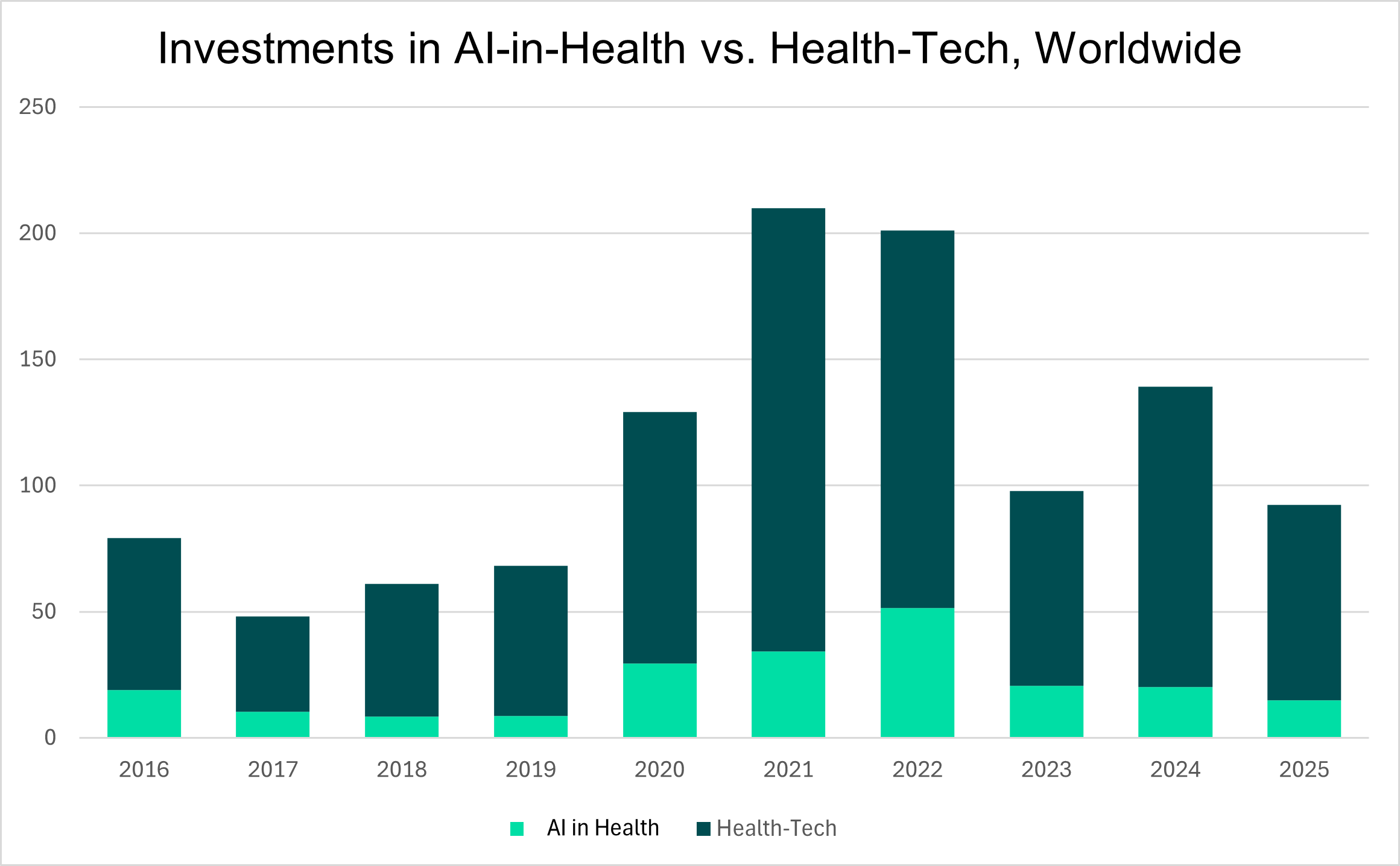

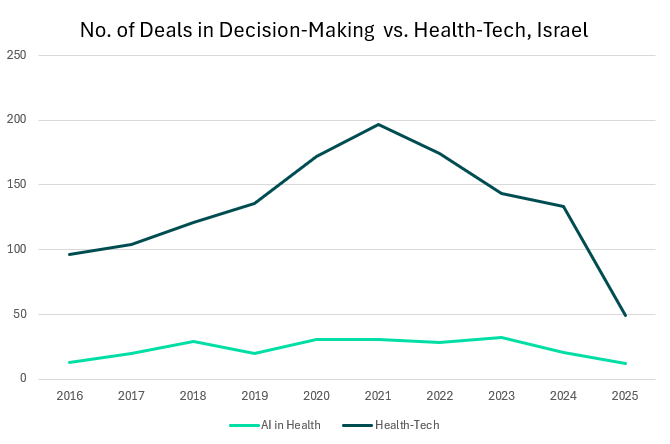

Global Investments in AI and Healthcare

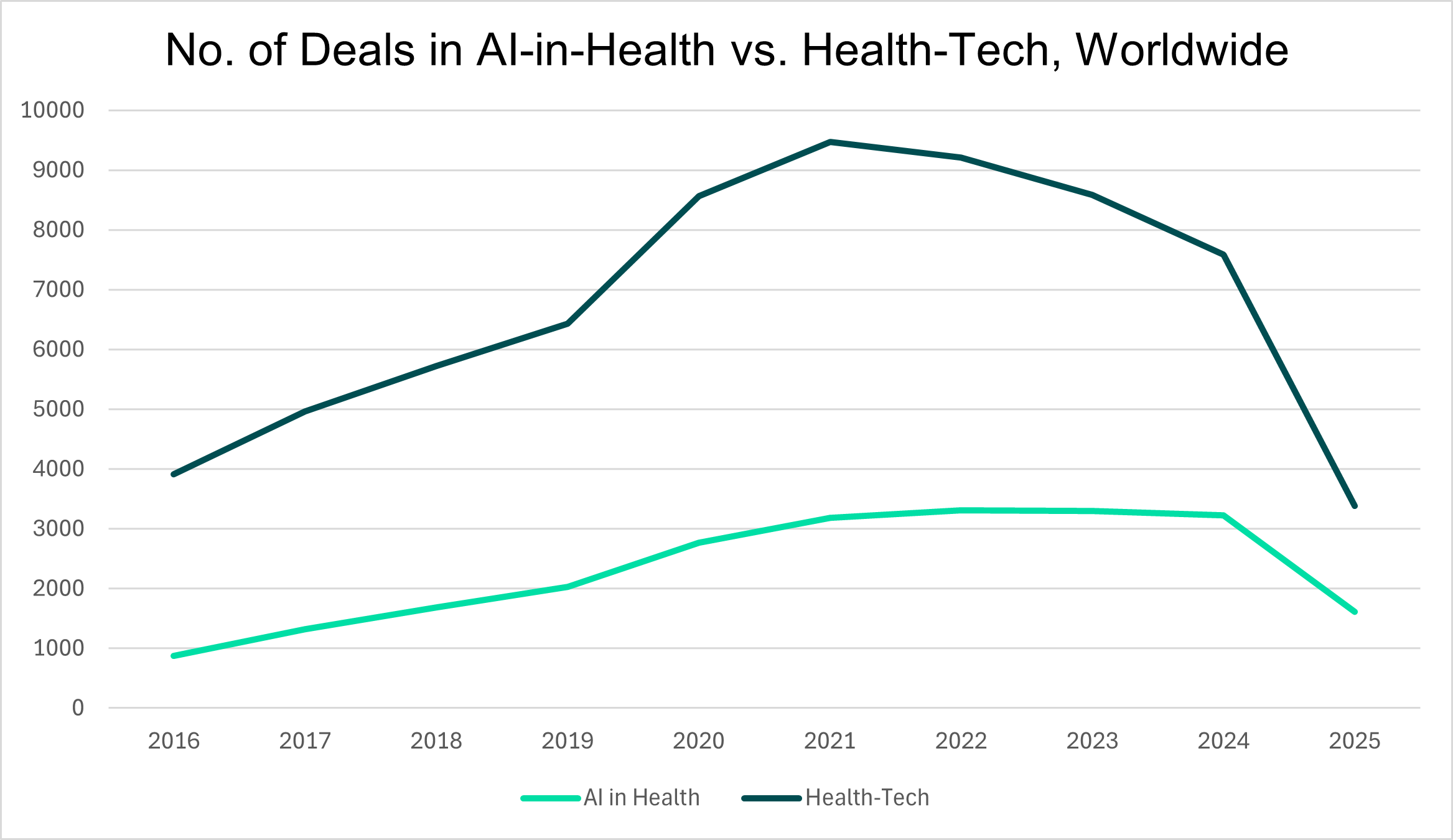

To assess global confidence in AI technologies in healthcare, worldwide investments in the field were examined. According to PitchBook, 8,314 active companies are integrating AI technologies in healthcare, with a total investment volume of approximately $238.7B. A gradual increase in deal activity began in 2016, slowing slightly in 2024 (2025 data was excluded due to incompleteness). Investment growth accelerated in 2018, reaching a peak in 2022, followed by significant declines in 2023 and 2024, despite major technological advances in AI during those years.

Trends in health technologies (HealthTech) more broadly – which include AI in healthcare – do not necessarily align with those specific to AI in healthcare. For example, between 2021 and 2022, while the total number of HealthTech deals declined, AI-related healthcare deals increased, indicating a focused preference and growing interest in this specific field.

PitchBook Data Analysis

The following table summarizes the global landscape of companies operating in AI and healthcare compared to the broader HealthTech sector. The data shows that AI in healthcare accounts for approximately 29% of all HealthTech companies worldwide and about 22% of total investments, reflecting a significant yet not dominant share.

The average investment per AI company is about 24% lower than the overall HealthTech average. In comparison, the deal rate is higher (30%), indicating a high level of activity but lower capital per company.

The United States clearly leads both in the number of companies and in total investment volume, followed by China, the United Kingdom, Canada, and India. Although Israel is not among the top five countries in terms of company count, it stands out with a high proportion of AI investments within HealthTech (around 29%), suggesting a focused specialization and prioritization of the field.

| AI in Healthcare | HealthTech | AI in Healthcare as % of HealthTech | |

|---|---|---|---|

| Total Companies | 8,314 | 28,837 | 28.80% |

| Total Investments ($) | 238.7B | 1.09Tn | 21.90% |

| Average Investment per Company ($) | 28,710 | 37,799 | 75.90% |

| Number of Deals | 26,532 | 87,982 | 30.20% |

| Largest Deal ($) | 18.8B | 28.2B | 17.10% |

| Number of Exits | 1,212 | 7,568 | 16% |

| Top Countries by Number of Companies | United States (2,920) China (505) United Kingdom (473) Canada (259) India (273) | United States (11,324) China (877) United Kingdom (1,362) Canada (1,048) India (889) | United States (25.8%) China (57.6% United Kingdom (34.7%) Canada (24.7%) India (30.7%) |

| Top Countries by Total Investments ($) | United States (191.8B) China (13.9B) United Kingdom (9.8B) Israel (3.7B) Canada (2.4B) | United States (854.6B) China (37.7B) United Kingdom (29.6B) Israel (13B) Canada (20.1B) | United States (22.4%) China (36.9%) United Kingdom (33.1%) Israel (28.5%) Canada (11.9%) |

Global Comparison Table – AI in Healthcare vs. Overall HealthTech Sector (PitchBook Data)

![]()

Global Regulation

The integration of AI tools into healthcare faces several challenges, including significant short-term regulatory barriers:

- A growing regulatory gap exists between countries leading AI governance and those lacking resources, potentially deepening existing inequalities in healthcare and weakening under-resourced systems.

- The pace of regulatory development is slower than the evolution of AI technologies, which delays innovation.

- Current software and AI regulations do not address GenAI, highlighting the need for targeted frameworks specific to generative technologies.

- There remains a significant challenge in data sharing and standardization across healthcare institutions, leading to issues related to privacy and data security.

AI Regulation in the United States and Europe

AI Regulation in the United States and Europe

In the United States, the FDA regulates medical AI, focusing on software safety, performance, and documentation of algorithmic updates. The agency plans to expand oversight of adaptiveAI systems and strengthen accountability and transparency, while investing in regulatory science research.

In the European Union, the AI Act defines risk levels for medical applications and imposes strict data privacy requirements. Plans include tighter clinical supervision and the development of enforcement standards, supported by Horizon Europe investments from the European Commission.

As part of this study, FDA-approved companies and technologies were analyzed to characterize the field and its regulatory landscape. As of May 2025, there are 1,016 FDA-approved AI systems across approximately 450 companies. The majority of approvals are in radiology (777; 76.5%), followed by cardiology (104; 10.2%) and neurology (42; 4.1%).

Ten companies account for 29% of total approvals (297), each holding at least ten FDA certifications, indicating potential leadership in the field. Among these, five are global corporations (e.g., GE Medical Systems, leading with 71 approvals), two are U.S.-based (e.g., iSchemaView with 15), two are Israeli (Aidoc Medical with 25; Viz.AI with 11), and one is Chinese (Shanghai United Imaging Healthcare with 25).

Broader regulatory and strategic developments are also emerging at the national and governmental levels, often serving as catalysts for advancing AI adoption in healthcare – these will be presented in the following section.

![]()

Government Support for AI Integration in Healthcare

To assess the role of governmental support in advancing the adoption of AI in healthcare, this section reviews national activities in the United States and the United Kingdom.

In the United States, the use of AI in medicine is expanding. As noted earlier, the FDA has approved more than 1,000 AI-powered medical devices as of April 2025. These systems typically focus on specific tasks – sometimes replacing the work of specialists, though not physicians entirely. Examples of systems that substitute for expert functions (as defined by their developers) include LumineticsCore and AEYE-DS for diagnosing diabetic retinopathy, DermaSensor for detecting skin cancer, the Viz LVO platform for stroke detection, and ProFound AI for mammography analysis.

In the United Kingdom, the government promotes AI integration through the National Health Service (NHS) to enhance efficiency and address workforce shortages. National policy aims to support rather than replace healthcare professionals through automation. In 2024, the NHS budget allocated £3.4 billion to digital transformation (including AI), targeting a 2% efficiency increase and projected savings of £35 billion. This budget also includes investments in global health-related technology companies.

On the regulatory front, the United Kingdom has implemented several vital measures: a pilot program aimed at providing recommendations for the use of AI in healthcare, with an emphasis on identifying risks and system biases before deployment and before using NHS data; the advancement of regulation for AI as a medical tool, reflected in the AI Airlock sandbox; and collaboration among national health authorities, such as NICE and MHRA, to develop recommendations and regulatory guidelines for AI-based medical products. Notable national initiatives include:

- Collaboration with Google DeepMind to develop an AI system for analyzing Optical Coherence Tomography (OCT) scans and diagnosing retinal diseases.

- Clinical decision support – the NHS launched a primary AI-based breast cancer diagnostic trial, analyzing about 700,000 mammograms to assess the accuracy of AI compared with radiologists.

- The NHS announced several physician support initiatives, including a tool designed to reduce administrative workload in healthcare, and the integration of VR and AR technologies for training and education of patients and staff, as well as for rehabilitation and clinical management.

![]()

Barriers in Israel and Worldwide

A 2023 study found that 44% of respondents expressed willingness to trust AI in healthcare, reflecting acknowledgment of its potential benefits alongside concerns about implementation and oversight. However, the integration of AI in healthcare is not yet guaranteed, due to fears of misinformation and data quality. This sentiment is echoed in the mixed attitudes observed across different regions: more than 40% of respondents in various Western countries expressed concern about AI integration in healthcare, compared with less than 20% in countries in Asia and South America.

The following are key barriers to implementing AI and granting it full autonomy in healthcare:

Regulation and Ethics

- AI technologies are often advancing faster than regulators can keep pace, particularly in diagnostics, disease prediction, and decision-making.

- The complexity of AI in healthcare can discourage policymakers and business leaders.

- Public officials often struggle to effectively integrate technology into their healthcare strategies, partly due to limited familiarity with technical aspects, leading them to delegate purely technical decisions to CTOs and other experts.

- In Israel: The Ministry of Health has not yet established comprehensive regulations for clinical AI use, though relevant processes are currently under development.

Accessibility and Quality of Medical Data

- AI models require clean, consistent, and high-quality data, yet significant difficulties are expected due to outdated medical records or fragmented systems.

- In Israel: While medical data repositories are generally strong, challenges remain in data interoperability and standardization across institutions. Additionally, some population groups are underrepresented in existing datasets.

Cultural Resistance and Systemic Conservatism

- Medical teams may resist AI adoption due to concerns about loss of responsibility, reduced authority, or difficulty adapting to change.

- The general public may also oppose automation, particularly when government leaders express skepticism or low confidence in such technologies.

- In Israel: Public trust in technology is relatively high, yet cultural change remains a barrier in large public systems. There is a prevailing view that AI should be integrated into healthcare only after proper regulation is established to prevent potential harm.

Economic and Infrastructural Barriers

- Developing and implementing AI systems requires substantial investment and skilled professionals – a challenge for countries with limited budgets.

- Collaboration between government and local stakeholders is often tricky, hindering large-scale technology adoption.

- In Israel: Many developments occur within the private sector. Hospitals and health funds actively promote AI integration, investing in both funding and training. A notable example is The Institute, a non-profit organization established in 2024 to support AI adoption in Israel.

Privacy and Data Security

- AI implementation requires access to personal and sensitive data, demanding strict adherence to privacy, encryption, and regulatory standards.

- In Israel: The national security situation increases exposure to cyber threats, including in the healthcare sector, leading to a strong emphasis on data protection. The Ministry of Health published a document in 2018 outlining interim guidelines and rules for the use of health information.

![]()

The AI and Healthcare Ecosystem in Israel

Israel’s healthcare and AI sector includes over 600 companies. Of these, approximately 380 develop partial automation technologies, around 80 focus on AI-based decision-making technologies, and the remaining companies focus on AI applications in healthcare fields outside the scope of this review, such as medical research and pharmaceuticals.

As part of examining Israel’s healthcare and AI ecosystem, this study focuses on companies capable of developing fully automated (Decision-Making) technologies, as well as the regulatory and operational barriers they face. The peak year for new company formations was 2020, marking a sharp rise since 2014. After 2020, the number of new entrants declined, suggesting possible stagnation in the sector.

Of the identified companies, 60 are based in Israel and 20 abroad. This may indicate challenges in implementing such services in Israel. Most of these companies are still in early funding stages.

To assess the regulatory impact on the ability of these 80 companies to advance toward full automation, the study classified each company by its regulatory risk level. The analysis shows that most of the companies’ products are associated with a medium-to-high level of regulatory risk (84% of the companies). For instance, companies engaged in tumor diagnostics are considered high-risk due to the severe consequences of diagnostic errors. This analysis highlights the significant influence of regulatory barriers on product maturity.

![]()

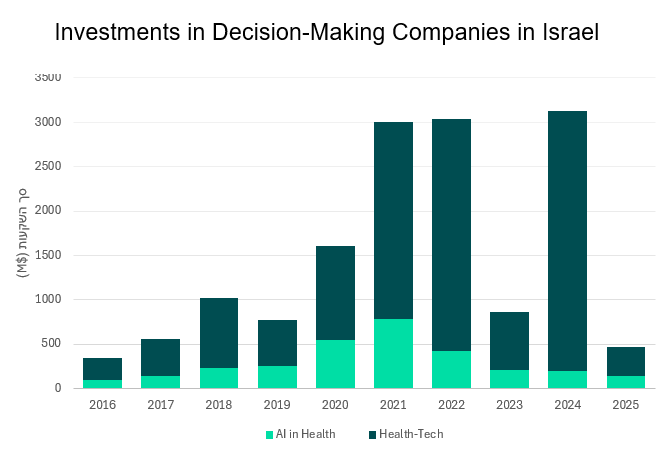

Investments in Decision-Making Companies in Israel

Based on PitchBook data, total investments in Decision-Making technologies within the healthcare and automation sectors amount to approximately USD 3.07 billion. Most of these investments occurred in 2021, followed by a noticeable decline in subsequent years. Compared with Israel’s overall health-tech sector, investment in Decision-Making technologies is relatively high, particularly in the number of companies, total investment volume, average investment per company, and number of investors.

PitchBook Data Analysis

The following table summarizes Israeli companies engaged in Decision-Making technologies in healthcare compared with those in the broader health-tech sector. The data show that Decision-Making companies represent a relatively small share of all health-tech firms (16.5%) but account for a larger portion of total investments – about 24%. The average investment per company is notably high (approximately USD 39 million, compared with USD 27 million in the overall sector), indicating strong investor interest and substantial fundraising despite the smaller number of companies. In the Decision-Making field, a relatively large number of investors are involved (around 36% of all health-tech investors), reflecting broad engagement and a strategic focus on automation.

| Decision-Making in Healthcare | Health-Tech (Total) | Decision-Making Share (%) | |

|---|---|---|---|

| Total companies | 79 | 479 | 16.50% |

| Total investments (USD) | 3.07B | 12.98B | 23.60% |

| Average investment per company (USD) | 38.9M | 27.1M | 143.50% |

| Number of deals | 295 | 1795 | 16.40% |

| Largest deal (USD) | 198M | 1.7B | 11.60% |

| Number of exits | 21 | 130 | 16.10% |

| Number of investors | 440 | 1228 | 35.80% |

Source: PitchBook ,Startup Nation Central and IVC Research Center

![]()

Regulation of Decision-Making Technologies in Israel

In Israel, as in other countries, there is growing governmental attention to developing AI regulation in general, and specifically for healthcare applications. In late 2023, a government policy paper was published outlining the principles of AI regulation. The document recommends aligning with the OECD guidelines on ethical principles for the development and use of AI. It also references a government decision to establish a Center for AI Regulation and Policy, intended to serve as a national knowledge and coordination hub for regulators and government ministries. This center was indeed founded in 2024. While the document does not address the healthcare sector specifically, it recommends advancing sector-based regulation (health, transportation, finance, etc.) rather than a single overarching framework.

With respect to AI in healthcare, the urgency for regulation stems from irregular and unsupervised uses of AI, which could have irreversible consequences. In late 2024, the Ministry of Health issued a Call for Comments on a draft document outlining principles for conducting clinical trials involving AI-based algorithms. The ministry’s objective is to identify key safety and ethical questions that must be addressed when evaluating the use of AI in interventional research.

Regarding FDA-related regulation, nine Israeli companies have received FDA approvals, totaling 60 approvals – approximately 6% of all global approvals in this field. These companies include those focused on radiology (for example, Viz.AI with 11 approvals and Nanox AI with three approvals) and those focused on diagnostics (for example, Healthy.io with four approvals and Tyto Care with three approvals).

![]()

Leading Israeli Companies in Decision-Making Technologies

The following companies have been identified as leaders in the field due to their high capital-raising volumes, technological innovation, global presence, public standing, or large workforce:

K Health – Uses patient learning models to display insights based on similar patient diagnoses.

Leading in total funding: USD 440.5 million.

Viz.AI – Specializes in brain disease detection, imaging analysis, and emergency alert systems.

Leading in funding: USD 289 million;

And in workforce size: 407 employees.

Concept Venus – Develops AI-based devices for rehabilitation, hair growth, and other aesthetic applications. Active in more than 60 countries.

Leading in funding: USD 288 million;

and in workforce size: 434 employees;

The company is publicly traded.

Aidoc – AI-driven platform providing real-time clinical insights and coordination across medical teams.

Leading in total funding: USD 284 million;

And in terms of workforce size, there are 450 employees.

Nanox AI – AI-based medical imaging solutions.

Leading in total funding: USD 270 million;

The company is publicly traded.

Tyto Care – AI-guided remote diagnostic platform enabling physical examinations both at home and in clinics.

Leading in total funding: USD 203 million.

![]()

Summary and Conclusions

This review highlights the depth of the global healthcare crisis – particularly the growing shortage of medical professionals, most evident in peripheral regions and particular specialties. Within this context, automation and AI technologies offer potential solutions. The technological developments are broad and impressive, including applications such as image-based diagnostics, autonomous monitoring, personalized treatment planning, clinical transcription and analysis, and more. However, most current AI tools function as decision-support systems, while only a small portion operate as decision-making systems with full or partial autonomy. In these cases, the technology can perform entire medical processes, though physical oversight by medical staff remains essential.

The investment landscape is similarly complex. On one hand, approximately 8,300 active AI-in-health companies exist globally, with a total investment volume of around USD 239 billion. On the other hand, 2023-2024 saw a significant decline in funding, despite notable technological progress. Countries that have established regulated testing environments – such as the UK (AI Airlock) and France (AI DReAM) – have not only accelerated innovation but also strengthened public and regulatory trust.

From an Israeli perspective, the potential is clear, but realization remains limited. Investments in AI-in-healthcare account for about 28% of total health-tech funding in Israel – a relatively high proportion compared to global figures – yet only a minority of companies operate in the decision-making domain. Moreover, Israel lacks formal regulatory frameworks or sandbox environments. While the country possesses high-quality medical data, advanced digital infrastructure, and a strong startup ecosystem, the absence of a unified policy prevents these assets from forming a clear competitive edge.

In conclusion, the successful integration of AI in healthcare requires more than technology alone. It depends on cohesive regulation, public and institutional trust, and the ability to manage experimentation, implementation, and oversight transparently and responsibly. The potential is significant – in improving patient care, enhancing efficiency, and reducing workload – but realizing it demands a systemic, gradual approach, continuously reassessing the boundaries of technological autonomy.